Market Retreats Amid Government Crackdown on Defense Contractors

The Canadian Vanguard Stock Market Report – Wednesday January 7, 2026 Edition.

.

The Toronto Market

The S&P/TSX Composite Index declined by 271.53 points, or 0.84%, closing at 32,135.49 and ending a three-session advance. Despite the pullback, the index demonstrated underlying support, holding above the psychologically important 32,000 level. Although the TSX briefly slipped below this threshold for approximately ten minutes in mid-morning trading, buying interest emerged quickly, driving a recovery that stabilized the index through the close.

![]()

Today’s TSX Market Statistics

Market breadth was negative, with declining issues outpacing advancers on the TSX. A total of 1,252 stocks declined, while 951 advanced, resulting in a decliner-to-advancer ratio of 1.31:1, with 130 issues unchanged.

Internal momentum moderated compared with the prior session. The number of new 52-week highs fell to 238, down from 436 on Friday, while new 52-week lows edged lower to 25 from 28, indicating a cooling in upside participation rather than a broad-based deterioration.

Total trading volume reached 529.7 million shares, representing a 2% decline from the previous session’s 539.4 million shares. Despite the modest pullback, turnover remained above recent daily averages, suggesting continued investor engagement.

Toronto Market Wrap-Up Report

Market leadership narrowed notably during today’s session, with Healthcare and Utilities standing out as the only two sectors to close higher. In contrast, Financials, Energy, and Industrials underperformed, reflecting a broad risk-off tone. Technology stocks also finished in negative territory, while Basic Materials declined 0.46%. Notably, despite the sector-level weakness, several of the day’s strongest individual performers were industrial metal miners—highlighting a divergence between index-level pressure and selective commodity-driven strength. This pattern echoes recent sessions in which stock-specific fundamentals have outweighed broader sector trends.

The list of the TSX’s top fifteen performers displayed a well-diversified mix, including mining and resource stocks, a power generation company, small-cap financials, and one real estate name. One notable inclusion was Lithium Americas Corp. (TSX: LAC), which has appeared consistently among the top performers for six consecutive sessions. This sustained presence suggests continued investor appetite for industrial and energy-transition metals, consistent with the elevated interest seen across the materials space over recent weeks. A key observation from today’s list is that all fifteen top performers were small-cap stocks, reinforcing the theme of selective risk-taking even as broader market breadth weakened.

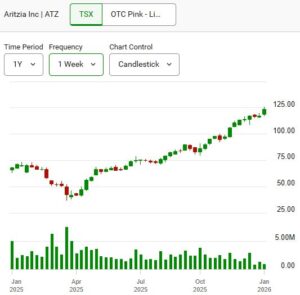

Within the manufacturing and retail space, Aritzia Inc. (TSX: ATZ) remains a stock to monitor closely in the near term ahead of its earnings release scheduled for tomorrow, January 8. The company’s shares have demonstrated strong momentum, and a results-driven catalyst could trigger a technical breakout if expectations are met or exceeded. Aritzia closed today up 2%, or $2.40, at $123.80, with trading volume of 859,200 shares.

From a historical perspective, Aritzia’s recent performance underscores the stock’s significant re-rating. On April 9, 2025—approximately nine months ago—ATZ closed at $45.77 with 1.55 million shares traded. The move to today’s close of $123.80 reflects a substantial appreciation, supported by improving fundamentals and growing analyst confidence.

Dejardins Securities currently rates the stock a Buy and raised its price target to $133.00 on January 6, while Raymond James increased its target to $130.00 yesterday and maintained an Outperform rating. This progression in analyst targets highlights the market’s evolving expectations and reinforces ATZ’s position as a standout name within Canadian discretionary equities.

.

The US Markets

U.S. Market Indexes

U.S. equity markets delivered a mixed performance, with downside pressure concentrated in blue chips and small caps, while technology shares provided limited support. The Dow Jones Industrial Average declined 466.00 points, or 0.94%, closing at 48,996.08. The S&P 500 slipped 23.89 points, or 0.34%, to finish at 6,920.93. In contrast, the Nasdaq Composite advanced 37.10 points, or 0.16%, ending the session at 23,584.27 and extending its winning streak to three consecutive sessions.

The Russell 2000 fell 7.47 points, or 0.29%, to close at 2,575.42. While today’s pullback marked a moderation from the stronger advances seen on Monday and Tuesday, small-cap equities continue to outperform on a week-to-date basis. Notably, the Russell 2000 finished second only to the Nasdaq, which was the sole major index to post a gain during the session.

However, the Nasdaq’s advance was relatively modest—approximately 20% of the prior session’s gain—underscoring the broader risk-off tone that characterized today’s trading and highlighting investor selectivity within growth-oriented names.

Today’s U.S. Market Statistics

New York Stock Exchange (NYSE): Market breadth on the NYSE was negative, with declining issues outpacing advancers. A total of 2,611 stocks declined, while 1,740 advanced, with 394 issues unchanged. This resulted in a decliner-to-advancer ratio of approximately 1.50:1, or roughly three decliners for every two advancers.

Internal momentum softened compared with the prior session. The NYSE recorded 410 new 52-week highs and 72 new 52-week lows, down from 583 new highs and 77 new lows reported yesterday, indicating a moderation in upside participation.

Total NYSE trading volume reached 5.29 billion shares, representing a 10% decline from the 5.81 billion shares traded in the previous session, consistent with the generally subdued risk appetite.

NASDAQ: Breadth on the NASDAQ also tilted negative, with declining stocks exceeding advancers. The exchange reported 2,628 decliners and 2,144 advancers, with 270 issues unchanged, producing a decliner-to-advancer ratio of 1.22:1, or approximately six decliners for every five advancers.

The NASDAQ posted 235 new 52-week highs and 75 new 52-week lows, compared with 293 new highs and 68 new lows yesterday, reflecting a pullback in momentum among growth-oriented names.

Total NASDAQ trading volume totaled 8.58 billion shares, down 3% from 8.82 billion shares traded in the prior session.

U.S. Market Wrap-Up Report

Wednesday’s trading session proved challenging, marked by early strength that faded by late morning and gave way to broad-based selling into the close. This intraday reversal was reflected in the divergence among major indexes, with the Dow Jones Industrial Average and the S&P 500 ending firmly in negative territory, while the Nasdaq Composite managed a modest gain—supported by selective strength in large-cap technology.

Sector performance underscored the cautious tone. Healthcare (+1.25%) and Technology (+0.10%) were the only two sectors to close higher, with the latter’s gain largely marginal. In contrast, Basic Materials, Industrials, Financials, and Utilities all declined by more than 1.2% on the session. Utilities (-2.34%) and Financials (-1.52%) were the weakest performers. The pronounced selloff in Utilities was particularly notable, as the sector typically attracts defensive flows during periods of heightened volatility—suggesting that risk reduction was broad rather than rotational.

This defensive breakdown was mirrored in market internals. On both the NYSE and NASDAQ, declining issues outpaced advancers, confirming the negative breadth underlying the day’s index-level performance. The contraction in new 52-week highs on both exchanges further signaled waning upside momentum compared with prior sessions, while relatively contained new lows suggested consolidation rather than capitulation. Trading volume declined on both exchanges, pointing to reduced conviction amid elevated uncertainty rather than panic-driven selling.

Volatility dynamics were consistent with this backdrop. While intraday swings increased—particularly during the late-morning selloff—the absence of a sharp volume spike indicates that investors remain selective rather than indiscriminately risk-averse. This environment continues to favor stock-specific positioning over broad beta exposure.

Financial stocks weighed heavily on the broader market, with major banks under pressure. Goldman Sachs declined approximately 1.5%, while Bank of America fell nearly 2.8%, contributing to the Dow’s underperformance and reinforcing the weakness seen across the financial sector.

Momentum-driven names also experienced a sharp reversal. Disk drive manufacturers, which had performed strongly since last Friday amid elevated demand from data center operators, saw that trend abruptly reverse. Seagate Technology Holdings (STX) declined 6.7%, while Western Digital Corp. (WDC) fell 8.9%. SanDisk Corporation (SNDK), the top S&P 500 performer on Tuesday, retreated intraday but managed to close up 1.12%, reflecting heightened volatility and profit-taking within the group.

Overall, the session was characterized by weakening breadth, moderating momentum, and rising selectivity—conditions that align with late-cycle or consolidation phases rather than outright risk capitulation.

NOTICE TO READERS

The Canadian Vanguard Stock Market is about empowering you to build and manage wealth by yourself. There is certainly no magic in managing finances or wealth but one needs to know what to do and commit to doing what is needed. When you are ready to start the journey to Put Your Destiny In Your Own Hands, read The Canadian Vanguard regularly, and if you wish to exchange ideas with a member of our team, please click Contact Us

Our readers are strongly advised to conduct their own research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is no guarantee of future price appreciation. Any recommendation is not a guarantee of any particular stock’s future prices, and The Canadian Vanguard accepts no responsibility or liability for investors’ or readers’ purchases.

Stocks In The News/ Stocks To Watch and Market Strategy will soon be available but only to Paying Subscribers.

(c) This article is published by The Canadian Vanguard on January 7, 2026