The Canadian Vanguard Stock Market Report – Weekend March 20 – 22, 2026 Edition

Equities Decline Amid Strong Sell-Off Driven by Rising Oil Prices and Geopolitical Concerns

. The Canadian Vanguard Stock Market Report is updated regularly during the weekend

.

The Toronto Market on Friday

The Toronto Market Index

The S&P/TSX Composite Index declined sharply by 437.57 points (-1.69%) to close at 31,317.41, reflecting broad-based selling pressure throughout the session. After opening modestly below the previous close, the index trended downward for most of the trading day, indicating sustained negative sentiment. While a late-session recovery attempt emerged, it lacked sufficient momentum to reverse intraday losses, suggesting limited buying conviction at lower levels.

From a broader perspective, the TSX had maintained a strong upward trajectory over the past year. The index’s close of 31,713 on December 30 marked a key inflection point, after which a sustained rally followed. This upward momentum culminated in a breakout above the 34,000 level on February 24, and a subsequent peak closing level of 34,541 on March 1. Notably, this peak coincided with the first trading session following the onset of the current Middle East conflict, highlighting a potential disconnect between geopolitical risk and short-term market resilience at that time.

The recent decline, culminating in a close near 31,319, indicates that the index has fully retraced its year-to-date gains. This development may signal a shift in market dynamics, with increased risk aversion, profit-taking, or reassessment of macroeconomic and geopolitical conditions contributing to the reversal. The inability to sustain levels above the 34,000 threshold and the speed of the retracement may also point to weakening technical support and heightened volatility in the near term.

![]()

Friday’s TSX Market Statistics

Market breadth on the TSX remained decisively negative. A total of 1,968 securities declined, compared to 313 that advanced, resulting in a decliner-to-advancer ratio of approximately 6.29:1. An additional 94 issues closed unchanged. This pronounced imbalance underscores persistent bearish sentiment and broad-based weakness across the market.

New 52-week lows continued to exceed new highs by a substantial margin. The exchange recorded 39 new highs and 145 new lows, compared with 66 new highs and 145 new lows in the previous session. While the number of new highs declined, the sustained elevation in new lows suggests continued downside pressure and limited participation in upward price movements.

Trading activity increased markedly, with total volume reaching 1,302,854,072 shares—representing a 97% increase from the 659,667,726 shares traded in the prior session. This sharp rise in volume, occurring alongside a significant price decline, is indicative of intensified selling pressure. Such volume-price dynamics are often interpreted as a sign of distribution, where market participants are actively exiting positions, reinforcing the prevailing bearish trend.

Friday’s Toronto Market Wrap-Up Report

The Toronto market ended the week on a notably weak footing, as the S&P/TSX Composite Index fell 437.57 points (-1.69%) to close at 31,317.41. Selling pressure persisted throughout the session, and despite a brief late-day recovery attempt, the index closed near its lows. Importantly, the TSX has now erased its gains for the year to date, reflecting a meaningful shift in market sentiment.

Market breadth remained decisively negative. Declining stocks outnumbered advancing stocks by more than six to one, highlighting broad-based weakness across sectors. At the same time, new 52-week lows continued to significantly exceed new highs, reinforcing the view that downside momentum remains firmly in place.

Trading volume surged sharply—up nearly 97% from the previous session. This combination of rising volume and falling prices suggests heightened selling activity, potentially driven by institutional repositioning and, in part, panic selling. This type of market behavior is typically associated with increased volatility and reduced investor confidence.

Several macroeconomic factors appear to be weighing on the market. Rising oil prices have contributed to renewed concerns about inflation, which may delay expected interest rate cuts. As higher interest rates tend to increase borrowing costs and pressure equity valuations, this environment remains challenging for stocks.

Sector performance was broadly negative, with nine of ten sectors closing lower. Technology and Basic Materials were among the weakest performers on the day. Over the course of the week, Energy was the only sector to post gains, while most others experienced moderate to significant declines—underscoring a clear risk-off tone in the market.

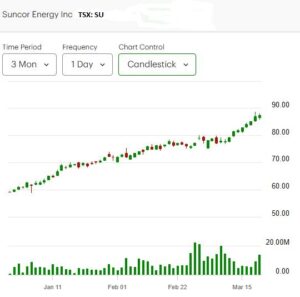

At the individual stock level, performance was mixed. Suncor Energy showed relative strength, supported by higher oil prices. Hammond Power Solutions Inc. also posted notable gains.

However, several previously strong performers, including Agnico Eagle Mines Ltd. and Wheaton Precious Metals Corp., moved lower, indicating a potential shift in leadership. Gold and precious metals’ prices have plummeted recently as investors flee save haven metals.

Investor Takeaway

Given the current market conditions, a cautious approach remains warranted. The combination of broad-based declines, rising volatility, and macroeconomic uncertainty suggests that capital preservation should be a priority. Maintaining disciplined risk management—including adhering to predefined exit strategies—can help navigate this more challenging environment.

Outlook for Next Week

Looking ahead, market direction will likely remain sensitive to movements in oil prices, inflation expectations, and interest rate outlooks. Continued volatility should be expected, particularly if geopolitical tensions persist or commodity prices remain elevated. Investors should watch for signs of stabilization in market breadth and trading volume, as these may indicate whether selling pressure is beginning to ease. Until clearer signals of support emerge, the near-term bias is likely to remain cautious, with downside risks still present.

Key Risks to Watch

Persistent inflation, elevated oil prices, and ongoing geopolitical uncertainty may continue to pressure equity markets and delay any near-term improvement in investor sentiment.

.

The US Markets

U.S. Market Indexes

All major U.S. equity indexes declined during the session, with small-cap stocks experiencing the most pronounced losses. The Dow Jones Industrial Average fell 443.96 points (-0.96%) to close at 45,577.47. The S&P 500 declined by 100.01 points (-1.51%) to 6,506.48, while the Nasdaq Composite dropped 443.08 points (-2.01%) to finish at 21,647.61. Markets opened below the prior session’s close and remained in negative territory throughout the trading day.

Although losses were initially moderate, selling pressure intensified in the early afternoon, leading to a broad-based and accelerated decline across all major indexes. This intraday deterioration reflects weakening investor sentiment and a lack of sustained buying support.

From a technical perspective, market conditions have weakened materially. All three major indexes are now trading below their respective 50-day moving averages and have also fallen below their 200-day moving averages. This alignment is typically viewed as a bearish signal, suggesting a potential shift toward a more sustained downtrend.

The Russell 2000 Index declined by 56.26 points (-2.26%) to close at 2,438.45, significantly underperforming large-cap benchmarks. The magnitude of this decline highlights increased pressure on smaller-cap equities, which are often more sensitive to tightening financial conditions and shifts in risk appetite.

Given the current technical breakdown and heightened volatility, a cautious investment stance remains appropriate. Elevated cash allocations may provide flexibility and risk mitigation during periods of market instability. Until clearer signs of technical stabilization emerge, prudence in initiating new equity positions is warranted.

Friday’s U.S. Market Statistics

Market breadth across U.S. exchanges remained firmly negative, with declining issues significantly outnumbering advancing issues.

On the New York Stock Exchange, there were 2,356 decliners compared to 428 advancers, resulting in a decliner-to-advancer ratio of approximately 5.54:1. An additional 39 issues were unchanged. This broad-based imbalance highlights continued selling pressure and weak market participation. New 52-week highs were minimal at just 1, while new lows totaled 4, compared with 103 highs and 173 lows in the prior session—indicating a notable contraction in upside momentum.

Trading activity increased significantly, with total NYSE volume reaching 10.41 billion shares, a 71% increase from the previous session. The combination of rising volume and declining prices suggests intensified distribution and increased selling pressure across the market.

On the NASDAQ Composite, market breadth was also negative, though somewhat less severe than on the NYSE. Decliners totaled 3,738 versus 1,126 advancers, resulting in a decliner-to-advancer ratio of approximately 3.32:1, with 148 issues unchanged. This still reflects a clear downside bias across the technology-heavy exchange.

New 52-week highs remained limited at 2, while new lows totaled 2, compared with 55 highs and 395 lows in the previous session. Although the number of new lows declined sharply from Thursday, the overall breadth continues to point to underlying weakness.

Trading volume on the NASDAQ rose to 12.16 billion shares, an increase of 40% from the prior day’s 8.74 billion shares. Similar to the NYSE, the increase in volume alongside declining prices suggests elevated selling activity and continued market stress.

Overall, market internals across both exchanges reinforce a risk-off environment, with broad participation on the downside and elevated trading activity pointing to increased volatility and distribution.

Today’s U.S. Market Wrap-Up Report

U.S. equity markets continued to exhibit weakness, with broad-based declines across major indexes and persistently negative market internals. The session was marked by elevated selling pressure, as declining issues significantly outnumbered advancing issues on both the New York Stock Exchange and the NASDAQ Composite. Additionally, the increase in trading volume alongside falling prices suggests ongoing distribution and heightened investor caution.

Sector performance was mixed, with Financials showing relative outperformance compared to other sectors. However, despite this relative strength, many financial stocks remain below their 200-day moving averages, indicating that they are still in technically weak positions and may carry elevated risk. Continued trading below this key long-term trend line suggests that caution remains warranted even in comparatively stronger sectors.

Market conditions have also deteriorated on a broader basis, with major indexes recording declines for a fourth consecutive week. This sustained weakness reinforces the prevailing bearish tone and highlights the absence of strong buying support. The Nasdaq, in particular, remains under pressure, reflecting continued vulnerability in growth and technology-related stocks.

From a technical and macro perspective, current market behavior is being heavily influenced by external factors, including oil price volatility and geopolitical developments. These drivers have introduced an additional layer of uncertainty, often overshadowing company-specific fundamentals. As a result, stock price movements are increasingly being driven by macroeconomic and geopolitical considerations rather than underlying business performance.

Given these conditions, a cautious investment approach remains appropriate. Elevated market volatility, weakening technical trends, and broad-based selling pressure suggest that capital preservation should remain a priority. Until clearer signs of stabilization emerge, it may be prudent to limit exposure, particularly in higher-beta areas such as the technology sector.

NOTICE TO READERS

The Canadian Vanguard Stock Market is about empowering you to build and manage your wealth by yourself. There is certainly no magic in managing finances or wealth but one needs to know what to do and commit to doing what is needed. When you are ready to start the journey to Put Your Destiny In Your Own Hands, read The Canadian Vanguard every market day. If you need more information please Contact Us

Our readers are strongly advised to conduct their own research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is no guarantee of future price appreciation. Any recommendation is not a guarantee of any particular stock’s future prices, and The Canadian Vanguard accepts no responsibility or liability for investors’ or readers’ purchases.

Stocks In The News/ Stocks To Watch and Market Strategy will soon be available but only to Paying Subscribers.

(c) This article is published by The Canadian Vanguard on March 22, 2026