Market Momentum Builds on Strength in Blue Chips, Precious and Industrial Metals

The Canadian Vanguard Stock Market Report – Monday January 5, 2026 Edition.

.

The Toronto Market

The S&P/TSX Composite Index surged 336.58 points, or 1.06%, to close at 32,219.95, marking its second consecutive session of strong gains. The index outperformed all major benchmarks except the Dow Jones Industrial Average. In 2025, Toronto’s S&P/TSX Composite has been the top performer among the major North American market indices we track. There is little reason to expect a different outcome by the end of 2026, as precious and industrial metals are likely to remain critical throughout the year, continuing a trend seen during President Trump’s tenure in the United States.

![]()

TSX Market Statistics

Market breadth was decisively positive, with advancing issues significantly outnumbering decliners. A total of 1,686 stocks advanced versus 548 decliners, producing a strong advancer-to-decliner ratio of 3.07:1, while 110 issues finished unchanged. This level of breadth indicates broad-based participation rather than gains driven by a narrow group of stocks.

Momentum was further confirmed by a sharp expansion in new highs. The TSX recorded 385 new 52-week highs compared with just 28 new lows, a substantial improvement from Friday’s 143 highs and 33 lows. The widening gap between new highs and lows suggests strengthening upside momentum and improving investor confidence across multiple sectors.

Trading activity reinforced the bullish signal, with total volume rising to 584.6 million shares—an increase of approximately 55% from Friday’s 377.0 million shares. The combination of rising prices and sharply higher volume points to institutional participation and validates the durability of the advance. Overall, these statistics reflect a robust and conviction-driven market session, supportive of continued near-term strength barring a deterioration in macro or commodity-related drivers.

.

The US Markets

U.S. equities posted strong gains across the board, led by cyclical and small-cap stocks. The Dow Jones Industrial Average climbed 594.79 points, or 1.23%, to close at 48,977.18, reflecting sustained buying interest throughout the session. The index opened roughly 100 points above the prior close, accelerated early in the trading day, and held near its intraday highs—an indication of steady institutional demand rather than late-session short covering.

The S&P 500 advanced 43.58 points, or 0.64%, ending at 6,902.05, while the Nasdaq Composite rose 160.19 points, or 0.69%, to finish at 23,395.82. Gains in the broader market suggest continued investor confidence in earnings resilience, even as leadership remains diversified rather than concentrated solely in mega-cap technology.

Small-cap stocks significantly outperformed. The Russell 2000 surged 39.70 points, or 1.58%, to close at 2,547.92, marking a second consecutive record-high session. As the strongest-performing index of the day, the Russell’s breakout underscores a growing risk-on appetite and increased expectations for domestic economic strength, easing financial conditions, or improved earnings leverage among smaller companies.

From an investment standpoint, the rotation toward small caps and industrial-heavy indices such as the Dow may signal a broadening of the market advance. If sustained, this trend could support a more durable bull market structure, particularly if accompanied by stable interest rates and continued economic momentum.

Today’s U.S. Market Statistics

New York Stock Exchange (NYSE): Market breadth was strongly positive, with advancing issues decisively outnumbering decliners. The NYSE recorded 3,406 advancers versus 1,144 decliners, while 341 issues finished unchanged. This produced a robust advancer-to-decliner ratio of 2.97:1, indicating broad participation in the market advance rather than gains concentrated in a limited number of stocks.

Momentum strengthened further as the exchange posted 583 new 52-week highs against just 77 new lows, a sharp improvement from Friday’s 236 new highs and 95 new lows. The expanding gap between new highs and lows signals accelerating upside momentum and improving underlying market health.

Trading activity confirmed the bullish tone. Total NYSE volume reached 5.81 billion shares, representing a 36% increase from Friday’s 4.27 billion shares. Rising prices accompanied by higher volume suggest increased institutional involvement and conviction behind the move.

NASDAQ: Breadth on the NASDAQ was also firmly positive. Advancing stocks totaled 3,458 compared with 1,362 decliners, with 261 issues unchanged, resulting in an advancer-to-decliner ratio of 2.54:1. This reflects solid participation across growth and technology-oriented names, even as leadership broadened beyond mega-cap stocks.

The NASDAQ recorded 293 new 52-week highs and 68 new lows, a notable improvement from Friday’s 130 highs and 118 lows. The reversal toward a higher high-to-low ratio points to renewed momentum and stabilization in growth sectors.

Volume expanded meaningfully, with total NASDAQ trading reaching 8.82 billion shares—up 17% from Friday’s 7.52 billion shares. The combination of positive breadth, expanding highs, and rising volume supports the view that the current advance is being reinforced by broad investor participation.

Overall, today’s market statistics point to a conviction-driven rally characterized by strong breadth, accelerating momentum, and volume confirmation—conditions that are typically supportive of continued near-term strength ahead of more detailed sector-level analysis.

Market Wrap-Up

U.S. equity markets delivered a broad-based and conviction-driven advance on Monday, supported by strong index performance, improving market breadth, and rising trading volume. Leadership extended beyond mega-cap growth, signaling a healthier and more durable market structure.

The Dow Jones Industrial Average led the major benchmarks, gaining 594.79 points (+1.23%) and closing near its intraday highs—an indication of sustained buying pressure throughout the session. The S&P 500 rose 0.64%, while the Nasdaq Composite advanced 0.69%, reflecting continued participation from growth-oriented names. Small caps significantly outperformed, with the Russell 2000 surging 1.58% to a second consecutive record close, underscoring a pronounced risk-on tone and growing confidence in the domestic economic outlook.

Market Breadth and Participation

Underlying market statistics reinforced the strength of the advance.

On the New York Stock Exchange, advancing issues overwhelmingly outpaced decliners, with 3,406 advancers versus 1,144 decliners and 341 unchanged. The resulting advancer-to-decliner ratio of 2.97:1 points to broad participation rather than index gains driven by a narrow group of stocks. Momentum strengthened further as the NYSE recorded 583 new 52-week highs against just 77 new lows, a sharp improvement from Friday’s readings. Trading volume rose 36% to 5.81 billion shares, confirming institutional engagement and reinforcing the credibility of the move.

The NASDAQ also posted solid internal strength. Advancers totaled 3,458 compared with 1,362 decliners, producing an advancer-to-decliner ratio of 2.54:1, with 261 issues unchanged. New 52-week highs expanded to 293 while new lows fell to 68, signaling improving momentum within growth and technology segments. Volume increased 17% to 8.82 billion shares, supporting the view that buyers remained active across the exchange.

Sector Leadership and Notable Movers

From a sector perspective, Basic Materials and Financials emerged as the top-performing groups, reinforcing the theme of rotation toward cyclical and economically sensitive areas of the market. Strength in these sectors aligns with expectations for sustained industrial demand, infrastructure activity, and stable financial conditions.

Several individual stocks stood out for both price action and volume confirmation:

-

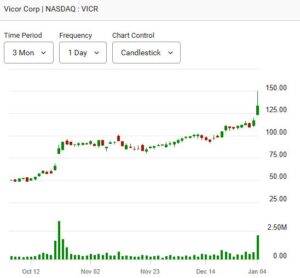

Vicor Corp. (VICR), a power component manufacturer, surged 14.36% on Monday after gaining 6.2% on Friday. The advance was accompanied by a 20% increase in trading volume on Friday, suggesting growing investor interest and momentum carryover.

-

FTAI Aviation (FTAI) continued its strong run, rising 7.42% Monday following a 6.86% gain on Friday. Notably, volume surged 158% on Monday after already increasing 71% on Friday, signaling aggressive accumulation and making the stock one to monitor closely.

-

Lam Research Corp. (LRCX), a key supplier of wafer fabrication equipment for the semiconductor industry, gained 5.24%, reflecting renewed strength within select areas of the technology and capital equipment space.

Outlook

Overall, the combination of strong index gains, expanding market breadth, rising volume, and leadership from cyclical sectors points to a broadening rally rather than a late-stage, narrowly led advance. While a more detailed sector analysis will follow, today’s data suggest improving market health and supportive conditions for continued near-term upside, provided macroeconomic and liquidity trends remain stable.

Investor focused Sector Rotation and Allocation Analysis

Monday’s market action points to an increasingly clear sector rotation underway, characterized by a shift toward cyclical, value-oriented, and economically sensitive sectors. Leadership from Basic Materials and Financials, combined with small-cap outperformance, suggests investors are repositioning portfolios in anticipation of sustained economic activity rather than defensive or narrowly growth-driven conditions.

Cyclical Leadership: Basic Materials

Basic Materials emerged as the strongest-performing sector, reflecting renewed confidence in industrial demand, infrastructure spending, and global supply-chain investment. Strength in this group typically coincides with expectations of stable or accelerating economic growth, particularly in manufacturing and construction-related activity. From an allocation perspective, continued leadership in materials supports overweight positioning in metals, mining, and specialty materials, especially where pricing power and balance-sheet strength remain intact.

The TSX’s heavy exposure to materials further reinforces this theme, creating cross-market confirmation between U.S. and Canadian equities. Unless commodity prices experience a sharp reversal, this sector is likely to remain a core driver of relative performance.

Financials: Confirmation of Risk Appetite

Financials ranked as the second-best-performing sector, signaling improving sentiment toward credit conditions, loan growth, and capital markets activity. Sector strength suggests investors are increasingly comfortable with the interest-rate outlook and see limited near-term stress in balance sheets. Banks and diversified financials tend to benefit from rising economic activity and increased transaction volumes, making them a natural beneficiary of a broadening expansion.

From a portfolio standpoint, leadership in financials supports increased exposure to well-capitalized institutions and select insurers, particularly those with leverage to domestic growth rather than international macro risk.

Technology: Rotation, Not Rejection

While technology did not lead the market, gains in the Nasdaq and strength in capital equipment names such as Lam Research (LRCX) indicate that investors are rotating within the sector rather than exiting it altogether. Hardware, semiconductor equipment, and infrastructure-related technology appear to be regaining traction, contrasting with more valuation-sensitive software and mega-cap growth names.

This internal rotation favors selective exposure to technology subsectors tied to capital investment, automation, and long-term secular demand, while encouraging more disciplined positioning in richly valued segments.

Industrials and Small Caps: Broadening Market Structure

The outperformance of the Dow Jones Industrial Average and the Russell 2000 underscores growing confidence in domestic economic momentum. Industrials benefit directly from increased capital spending, infrastructure activity, and reshoring trends, while small-cap stocks reflect improving earnings leverage and reduced risk aversion.

Sustained leadership in small caps typically marks an early-to-mid expansion phase rather than a late-cycle environment. For asset allocators, this supports incremental rebalancing toward domestically focused cyclicals and away from overly concentrated large-cap exposure.

Allocation Implications

Taken together, the current rotation favors:

-

Overweight: Basic Materials, Financials, Industrials, and select Small Caps

-

Neutral to Selective Overweight: Technology (with emphasis on capital equipment and infrastructure-related segments)

-

Underweight or Selective: Defensive sectors unless volatility re-emerges

If breadth, volume, and new-high metrics remain supportive, this rotation could persist, reinforcing a market structure built on diversified leadership rather than narrow concentration. Confirmation will depend on stable interest rates, commodity price trends, and continued earnings resilience.

Commodities and Bonds

Oil Price: Crude Oil futures was down -0.20% at $58.1298 per barrel, as of the time (11:30 pm EST, Monday) of this post update.

Gold price is up $25.50, or 0.58%, at $4,476.70 per troy ounce, while silver price is up $2.12, or 2.77%, at $78.78 per ounce as of the time of this post update.

Bitcoin (BTC-USD) was trading down -$749.80 or 0.80% at $93,533.00 as of the time of this post update.

10 –year Treasury Yield: The 10-year Treasury yield was at 4.179%, as of the time (11:30 pm EST, Monday) of this post update.

After-hours action: Futures are little changed Monday evening though Dow Jones index was a record high earlier during the day. Dow futures is up 14.00 points or 0.03% vs. fair value. S&P 500 futures is up 12.00 points or 0.03% at 6,955.50 and Nasdaq 100 futures is up 82.75 points or 0.32% at 25,661.00 as of the time (11:30pm EST, Monday) of this post update.

Reminder: Overnight futures often have little correlation to the following day’s regular trading session. All figures reflect market conditions at the time of capture only.

NOTICE TO READERS

The Canadian Vanguard Stock Market is about empowering you to build and manage wealth by yourself. There is certainly no magic in managing finances or wealth but one needs to know what to do and commit to doing what is needed. When you are ready to start the journey to Put Your Destiny In Your Own Hands, read The Canadian Vanguard regularly, and if you wish to exchange ideas with a member of our team, please click Contact Us

Our readers are strongly advised to conduct their own research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is no guarantee of future price appreciation. Any recommendation is not a guarantee of any particular stock’s future prices, and The Canadian Vanguard accepts no responsibility or liability for investors’ or readers’ purchases.

Stocks In The News/ Stocks To Watch and Market Strategy will soon be available but only to Paying Subscribers.

(c) This article is published by The Canadian Vanguard on January 5, 2026