The Canadian Vanguard Stock Market Report Weekend April 24-26, 2026 Edition

Nasdaq Hits Record High as Markets Advance on Strong Earnings and Optimism Over U.S.–Iran Ceasefire Talks

The Canadian Vanguard Stock Market Report is updated regularly during the weekend

.

The Toronto Market

Friday’s Toronto Market Index

The S&P/TSX Composite Index slipped 8.82 points (-0.03%) on Friday to close at 33,904.11. The index opened below Thursday’s close but recovered by midday to reach that level. It then traded largely sideways for the remainder of the session before dipping slightly in the final minutes to end just below the previous close.

Trading volume declined significantly, coming in about 20% lower than Thursday’s level. The TSX remains approximately 1.8% below its 52-week high.

Overall, the Toronto market continues to show strength, maintaining solid conditions for both investing and trading.

![]()

Friday’s TSX Market Statistics

On Friday, the S&P/TSX Composite Index showed positive market breadth, with advancing issues outnumbering declining ones. There were 1,278 advancers compared to 811 decliners, resulting in an advancer-to-decliner ratio of 1.57 to 1—roughly three advancers for every two decliners. An additional 137 issues remained unchanged.

The exchange recorded 181 new 52-week highs and 23 new 52-week lows, compared with 161 new highs and 25 new lows in the previous session.

Total trading volume reached 389,787,893 shares, representing a decline of approximately 20% from Thursday’s 492,131,956 shares. Notably, Thursday’s volume had been about 20% higher than Wednesday’s, indicating some recent fluctuation in trading activity.

Recent market movements appear influenced by geopolitical developments, particularly tensions involving the United States and Iran, which can contribute to periods of heightened volatility and occasional overreactions by investors.

Friday’s Toronto Market Wrap-Up Report

The S&P/TSX Composite Index edged lower on Friday, marking its second consecutive down session, though the decline remained marginal. Despite this short-term softness, the index continues to close higher more often than lower, reflecting an underlying positive trend.

Healthcare led the market on Friday, followed by Consumer Discretionary (Durable Consumer Goods & Services), which gained 0.94%, and Industrials, up 0.30%. On the downside, Energy fell 0.57% and Telecommunications declined 1.63%, making them the session’s laggards. Financials were essentially flat, up just 0.04%, while Technology slipped 0.14%.

Sectors This Week:

Healthcare was the top-performing sector for the week, rising 4.30%. Energy advanced 2.91%, Telecommunications Services gained 2.61%, and Industrials moved higher by 1.77%. In contrast, Consumer Discretionary declined 1.25%, while Technology (-4.66%) and Basic Materials (-5.54%) were the weakest sectors.

Company Highlights:

Within the Technology sector, Celestica Inc. stood out, rising 4.38% to close at $561.00 on volume of 553K shares. In Energy, Precision Drilling Corporation gained 3.41% to close at $130.18, with 72.8K shares traded. Although trading volume in PD fell below the preferred 100K-share threshold, it remains a stock to watch in the near term given current market conditions.

Market Analysis & Outlook

Market breadth remained positive, with advancers outpacing decliners, suggesting underlying resilience despite the index’s slight pullback. However, declining trading volume—down roughly 20% from the previous session—points to reduced conviction among market participants.

Sector rotation was evident this week, with capital flowing into defensive and healthcare names while Technology and Basic Materials experienced notable weakness. This pattern often reflects a more cautious market tone.

Geopolitical tensions, particularly involving the United States and Iran, continue to influence investor sentiment. These developments are contributing to heightened volatility, especially in Energy markets, where price swings can trigger short-term momentum trades and occasional overreactions.

From a tactical standpoint, the TSX remains close to its recent highs, indicating that the broader uptrend is still intact. However, the combination of lower volume, sector divergence, and external geopolitical risks suggests that traders should remain selective, focusing on strong sectors and liquid names while being mindful of sudden sentiment shifts.

.

The US Markets

Friday’s U.S. Market Indexes

The major U.S. indexes closed mixed on Friday. The Dow Jones Industrial Average slipped 79.61 points (-0.16%) to close at 49,230.71. In contrast, the S&P 500 gained 56.68 points (+0.80%) to end the session at 7,165.08, while the Nasdaq Composite advanced 398.09 points (+1.63%) to 24,836.60. The Russell 2000 Index also moved higher, rising 11.90 points (+0.43%) to close at 2,787.00.

Market performance continues to be influenced by geopolitical developments, particularly ongoing war-related news, which has contributed to uneven sector responses and heightened volatility. The Dow’s decline reflects relative weakness in more traditional and cyclical components, while strength in growth-oriented sectors has lifted the broader market.

Both the S&P 500 and Nasdaq Composite are trading at or near all-time highs, supported by a renewed rotation into technology stocks. This shift has been a key driver of recent market momentum, with semiconductor stocks leading the advance. Notably, Intel Corporation surged approximately 20% on Friday, highlighting strong investor demand within the chipmaking segment.

U.S. Friday Market Statistics

New York Stock Exchange (NYSE): Advancing issues outnumbered declining issues, indicating moderately positive market breadth. There were 1,516 advancers compared to 1,221 decliners, with 101 issues unchanged. This produced an advancer-to-decliner ratio of 1.28 to 1—approximately six advancers for every five decliners.

The exchange recorded just 2 new 52-week highs and 3 new 52-week lows. This marks a sharp decline from the previous session, which saw 301 new highs and 48 new lows, suggesting a significant cooling in upside momentum.

Total NYSE trading volume reached 4,716,147,166 shares, down 13% from 5,383,932,488 shares in the prior session, pointing to reduced participation and potentially weaker conviction among investors.

NASDAQ: At the NASDAQ, advancing stocks also outpaced declining stocks, reflecting stronger breadth than the NYSE. There were 2,845 advancers and 2,009 decliners, resulting in an advancer-to-decliner ratio of 1.41 to 1—roughly seven advancers for every five decliners. An additional 169 issues remained unchanged.

The exchange posted 3 new 52-week highs and no new lows, compared with 271 new highs and 81 new lows in the previous session. Similar to the NYSE, this sharp drop in new highs suggests a pause in broad-based breakout activity despite index-level strength.

Total NASDAQ trading volume rose to 10,493,067,905 shares, an increase of 28% from 8,176,107,148 shares traded in the prior session. This divergence—higher volume on NASDAQ versus lower volume on the NYSE—indicates that trading activity was more concentrated in growth and technology-oriented names.

U.S. Market Wrap-Up Report

Only four of the major sectors advanced on Friday. Technology led the market, gaining 2.40%. Consumer Discretionary (Consumer Goods & Services) rose 0.75%, Basic Materials added 0.55%, and Utilities edged higher by 0.12%. On the downside, Financials declined 0.42% and Industrials fell 0.55%, while Healthcare (-1.05%) and Telecommunications Services (-2.10%) were the weakest-performing sectors.

On a weekly basis, five sectors posted gains. Energy was the top performer, rising 3.36%. Technology followed with a 2.76% gain, while Telecommunications Services advanced 2.61% and Utilities climbed 2.33%. Financials (-2.38%) and Healthcare (-3.12%) were the weakest sectors for the week.

In company and industry highlights, semiconductor and chip manufacturers dominated market attention and performance on Friday. Taiwan Semiconductor Manufacturing Company surged 5.17% in New York, supported in part by regulatory changes in Taiwan allowing greater ETF investment in local companies. Intel Corporation also stood out, breaking out following a stronger-than-expected earnings report released after Thursday’s close; the stock jumped 15.79% on heavy volume of 284 million shares.

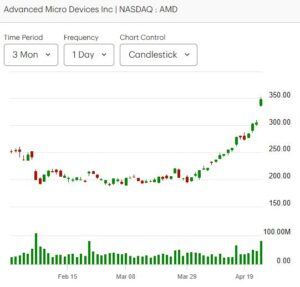

The strength extended across the semiconductor space. Arm Holdings Plc climbed 14.76% to close at $234.81 on 20.5 million shares traded, while Advanced Micro Devices rose 13.91% to $347.80 on 81.6 million shares. AMD has now advanced in four consecutive sessions and 12 of the last 14, reaching a new 52-week high of $352.99 on Friday.

Friday’s session was notably bullish, with the Nasdaq Composite hitting a new record high.

Market Interpretation (Breadth & Index Performance)

Despite mixed sector performance, overall market breadth remained positive, with advancers outpacing decliners on both the New York Stock Exchange and the NASDAQ. However, a sharp decline in new 52-week highs on both exchanges suggests that the rally is becoming increasingly concentrated rather than broad-based.

This narrowing leadership helps explain the divergence among major indexes. The technology-heavy Nasdaq Composite surged to new highs, driven by strong momentum in semiconductor stocks, while more diversified indexes showed comparatively muted performance. Increased trading volume on the NASDAQ, contrasted with lighter volume on the NYSE, further reinforces the view that capital is rotating aggressively into growth and technology names.

In summary, index strength—particularly in the Nasdaq—is being powered by a relatively small group of high-performing technology stocks rather than widespread participation across sectors. While this can sustain upward momentum in the short term, it may also increase the market’s sensitivity to sector-specific pullbacks.

Short-Term Trading vs. Long-Term Investment Perspective

From a short-term trading standpoint, momentum remains firmly in favor of technology and semiconductor stocks, with strong price action, rising volume, and breakout patterns—particularly in names like Advanced Micro Devices and Intel Corporation. Traders may continue to find opportunities by focusing on relative strength within these leading sectors, while remaining cautious of sudden reversals given elevated volatility and headline-driven market swings.

For long-term investors, the broader trend remains constructive, with major indexes near all-time highs and supported by earnings growth in key sectors. However, the current narrow leadership and sector divergence suggest the importance of maintaining diversification and avoiding overconcentration in high-momentum areas. A balanced approach—combining exposure to growth sectors like technology with positions in more stable or cyclical sectors—may help manage risk while still participating in the market’s upward trajectory.

.

NOTICE TO READERS

The Canadian Vanguard Stock Market is about empowering you to build and manage your wealth by yourself. There is certainly no magic in managing finances or wealth but one needs to know what to do and commit to doing what is needed. When you are ready to start the journey to Take Charge and Put Your Destiny In Your Own Hands, read The Canadian Vanguard every market day. If you need more related information, Contact Us

Our readers are strongly advised to conduct their own research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is no guarantee of future price appreciation. Any recommendation is not a guarantee of any particular stock’s future prices, and The Canadian Vanguard accepts no responsibility or liability for investors’ or readers’ purchases.

Stocks In The News/ Stocks To Watch and Market Strategy will soon be available but only to Paying Subscribers. The dollar sign “$” in the Toronto Market section in the articles only stands for Canadian dollar and in the US market section “$” stands for US dollar.

(c) This article is published by The Canadian Vanguard on April 25, 2026