Tariffs and market-related disruptions are here to stay, at least in the short term

The Canadian Vanguard Stock Market Report – Weekend June 6 – 8, 2025 Edition

. (The Stock Market Report is updated constantly through the weekend)

The Toronto Market

The TSX composite index gained 86.84 points or 0.33%, to close the session at 26,429.13. The TSX gained on Friday, but was the worst performer of the four North American major indexes that we report on every market day. However, the index remains the best performer of the four indexes over the past six weeks. The index has now gained in twenty one of the last twenty-four market sessions.

The Market Breadth

Five of the ten major TSX sectors gained on Friday. Technology, up 3.05%, was the clear top sector. There was a clear 2% difference in the gains between the sector and Healthcare, which gained just 1.00%. Energy was next with a 0.54% gain. Financials was up 0.54%, and Industrials was up 0.28%. Durable Consumer Goods & Services declined -0.09%; Telecommunications Services declined -0.26%; Utilities declined -0.59%; Discretionary Consumer Goods & Services declined -0.97%; and Basic Materials declined -1.34%.

Industry Groups: The top five industry groups in the TSX today were: Consumer Electronics, up 20.54%; Computer Hardware, up 5.84%; IT Services & Consulting, up 5.38%; Pharmaceuticals – Generic & Specialty, up 3.34%; and Insurance-Multiline, up 3.31%.

The Week’s Weekly Review: The weekly performance by the TSX sectors gives a good picture of the effects of tariff disruptions on the markets. TSX has been up a good number of times compared to the other North American indexes. However, the gains were small several times and the market breadth was always narrow. On a weekly basis this week, only five of the ten major sectors gained. Basic Materials, up 4.46%, was the top sector this week.

Gold was always up in market sessions following President Trump’s makes tariff announcements. Gold belongs to the Basic Materials sector. Energy gained 1.98% this week. Technology gained 3.05% today, but the sector was up a mere 1.29% for the week. Durable Consumer Goods & Services gained 0.66%, and Financials gained 0.59%. Healthcare was down -0.29%; Industrials was down -0.33%; Telecommunications Services was down -0.36%; Utilities was down -1.27%; and Discretionary Consumer Goods & Services declined -2.99% this week.

Today’s Statistics

Friday, the issues that gained (Advancers) outnumbered those that declined (Decliners). There were roughly three Advancers for every two Decliners, or a more exact ratio of 1.48-to-1.0. In real numbers, there were 1,135 Advancers to 765 Decliners while 122 stocks remained Unchanged.

Today, there were 134 new 52-Week Highs and 13 new 52-Week Lows. There were 144 new 52-Week Highs and 16 new 52-Week Lows on Thursday.

The total volume of shares traded at the TSX today was 403,723,054, or 7% less than the volume of 435,308,228 shares traded on Thursday.

The US Markets

The Dow Jones Average index advanced 443.13 points or 1.05% to close the session at 42,762.87. The S&P 500 index gained 61.06 points or 1.03% to close at 6,000.36. The Nasdaq Composite gained 231.51 points or 1.20%, to close at 19,529.95. In small caps, Russell 2000 advanced 34.89 or 1.66% to close at 2132.25.

The Market Breadth: Friday was a good market session for stocks, and as such, investors. The week had seen a very narrow breadth during most of the sessions earlier in the week, but Friday was different. Nine of the major sectors gained on Friday. Energy, up 1.51%, was the top sector on Friday. Durable Consumer Goods & Services gained 1.36%; Financials gained 1.16%; Healthcare gained 1.02%; and Technology gained 1.01% to round up the list of sectors which gained 1% or higher on Friday. Industrials gained 0.96%; Telecommunications Services was up 0.63%, and Discretionary Consumer Goods & Services was up 0.16%. Basic Materials, down -0.17%, was the laggard of the day and the only sector to end the session in the red.

Industry Groups: The top five industry groups in the US markets on Thursday were: Rails & Roads – Passengers, up 4.24; Oil & Gas Drilling, 3.87%; Airlines, up 3.28%; Retail – Catalog & Internet Orders, up 2.58%; and Oil & Gas Exploration & Production, up 2.58%.

The Week’s Weekly Review: It was a relatively positive week overall, as seven of the major sectors gained on a weekly basis this week. Healthcare was the top sector this week. The sector gained 5.75% this week. Technology followed with a weekly gain of 3.83%. Energy gained 2.49%; Basic Materials gained 2.24% this week; Industrials gained 1.48%, and Financials gained 1.37%. Retail sectors lagged this week. The bottom three sectors this week were Durable Consumer Goods & Services, down -0.07%; Utilities, down -0.59%; and Discretionary Consumer Goods & Services, down -0.91%.

Today’s Market Statistics

At the NYSE, the issues that gained (Advancers) outnumbered the issues that declined (Decliners). There were roughly two Advancers for every Decliner, or an exact ratio of 2.14-to-1.0. In actual numbers, there were 2,745 Advancers to 1,284 Decliners with 275 Unchanged.

Today, there were 174 new 52-Week Highs and 34 new 52-Week Lows. There were 253 new 52-Week Highs and 49 new 52-Week Lows on Thursday.

The total volume of stocks traded today at the NYSE was 4,427,984,484, or 15% less than the total volume of 5,175,656,657 shares traded on Thursday.

On the NASDAQ, the Decliners totally outnumbered the Advancers. There were roughly three Decliners for every two Advancers, or an exact ratio of 2.48-to-1.0. In actual numbers, there were 3,189 Decliners to 1,287 Advancers with 138 Unchanged.

Today, there were 173 new 52-Week Highs and 38 new 52-Week Lows. There were 164 new 52-Week Highs and 62 new 52-Week Lows on Thursday.

The total volume of shares traded at the NASDAQ today was 7,451,472,148, or 18% less than the total volume of 9,080,984,314 shares traded on Thursday.

Market Roundup Report

The markets were up and ended the session in green. However, the tariff disruptions are still very much around. On Friday, all the indexes gained, but the volumes of shares traded were down substantially for each of the exchanges. When the indexes are up and volumes of shares traded are down, that is evidence that the institutions are likely selling or not buying. Stock’s prices are not likely to go up and remain up when the institutions are not buying.

Oil Price: US oil futures rose today. Oil prices climbed to around $63.35 a barrel. US oil price was at $64.48 per barrel as of the time (11:30pm ET, Sunday) of this post update.

10 –year Treasury Yield: The US 10-year Treasury yield rose three basis points to settle above 4.39%. The 10-year yield was at 4.498% as of the time (11:30pm ET, Sunday) of this post update.

After-hours action: Futures were down slightly Sunday evening. Dow Futures was down -85.00 points or -0.21% vs. fair value. S&P 500 futures was down -14.25 or -0.24%, and Nasdaq 100 futures was down -60.75 or -0.28% as of the time (11:30 pm ET, Sunday) of this post update.

.

Regular Market Day Features

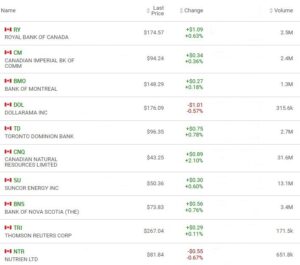

The Canadian Vanguard Beginner Investor’s Watchlist

The Canadian Big Six banks were all up on Friday.

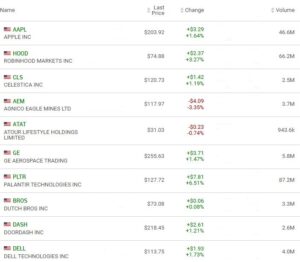

The Blended Growth Stock Watchlist

Apple Inc. (AAPL) may be staging a comeback, but the AI promise appears nowhere around the corner.

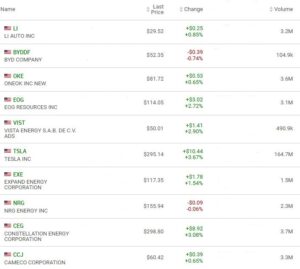

EV Manufacturers and Resource Stocks

NOTICE TO READERS

Our readers are strongly advised to conduct their own research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is no guarantee of future price appreciation. Any recommendation is not a guarantee of any particular stock’s future prices, and The Canadian Vanguard accepts no responsibility or liability for investors or reader’s purchases.

The Canadian Vanguard’s stock market reports, https://www.thecanadianvanguard.com/category/stock-markets/ are composed senior professional stock market industry and Information Technology professionals. We deliberately neither engage nor deploy AI tools to produce these reports.