Splitting the Bills: How the Real Estate Downturn is Forcing Former Partners to Share Homes

Brenda Trinh can’t recall exactly how long she and her ex remained under the same roof after the relationship began to unravel. But her concerns about money and the rental market made moving out more complicated.

Subconsciously, she said, those concerns might have played a role in how much longer they stayed together.

Ms. Trinh, 31, moved in with her partner during the pandemic, just before Toronto rents – and housing prices – skyrocketed. The couple initially split $1,800 a month in rent for their one-bedroom apartment before it climbed to $2,000.

When the relationship was ending, the potential expenses Ms. Trinh would face by living separately weighed on her.

“When you’re in a situation like that it’s very isolating and you feel vey alone – you can’t discuss it with your partner,” she said.

Ms. Trinh is among thousands of Canadians who have delayed finalizing the end of a relationship or even moving out after a relationship fell apart because they didn’t know if they could afford to live on their own, with many fearing being priced out of the housing market. A survey by the Bank of Montreal published last week found that one-third of Canadians feel financially pressured to move in with a partner in the first place.

BMO’s research was conducted by Ipsos from Dec. 29, 2025 to Jan. 27, 2026, across a sample of 2,503 adults in Canada.

For those who co-own property, softening housing market conditions in recent years have made living apart after ending the relationship even more challenging. In BMO’s survey, nearly two-in-five divorced or separated Canadians said the financial cost of those processes kept them together longer than they wanted.

Meanwhile, 28 per cent said they had delayed a legal separation or divorce, with 32 per cent of those participants citing the leading cause as concerns about financial costs of the process, and 27 pointing to the cost of affording separate households.

“We’re seeing more and more now, people who can’t afford to move out, even after they’ve decided: ‘Yes, we are separated, we have lawyers, and we are getting the separation process all started,’” Toronto divorce lawyer Justin Lee said.

The main fear for homeowners is often driven by a lack of equity built in the matrimonial home, and the prospect of selling at a steep loss. That’s coupled with worries around the costs of starting a new household from scratch – whether renting or buying – in an unpredictable market.

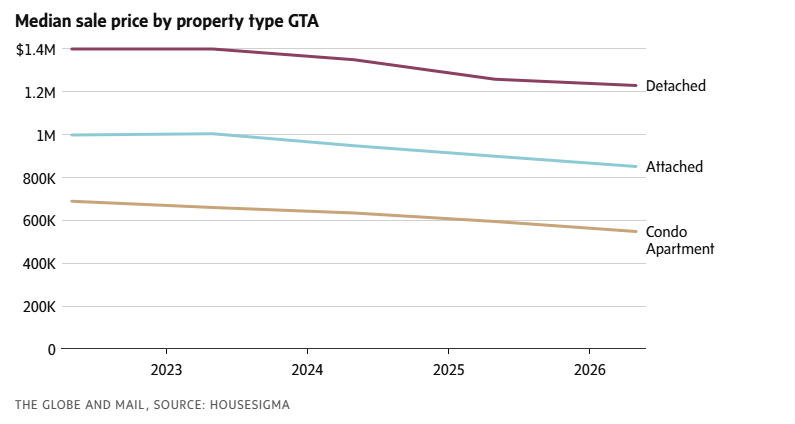

According to HouseSigma, the median GTA condo apartment sold for $548,000 in May, 2026, down 7.8 per cent – or about $47,000 – from last May. The price of detached homes dipped 2.3 per cent annually, while 74 per cent of all homes sold below list price.

But even those who have built some equity are hard-pressed to move, said Eva Sachs, a financial planner and certified divorce financial analyst. “It’s very difficult for a lot of people to digest that they worked so hard to buy a home, only to have to sell it and walk away with barely anything.”

Many are prepared to wait for market conditions to improve, she said. “The question is for how long.”

Disagreements over a home’s value, whether to sell and who should absorb potential losses have prolonged divorce negotiations in the last few years, said Roxana Soica, who works in family law. Buyouts – where one spouse purchases the other’s share of a home – have also become more difficult as those separating struggle to agree on fair valuations in a declining market.

There used to be “a lot of money left in the home for each party to have a good down payment for a new home,” Ms. Soica said.

Another flashpoint is mortgage renewals, said Stefanie Ricchio, a chartered professional accountant and financial literacy advocate. “Anyone renewing now is often facing a higher payment than they signed up for, which blows up whatever budget they’d assumed.”

While prices have eased for renters, the declines are often happening among studios and one-bedroom units, and less across bigger residences suitable to living there long-term, or for a parent with a child. While asking rents fell 3.2 per cent nationally between 2024 and 2025, average rent for a two-bedroom apartment grew 5.1 per cent, according to data from Rentals.ca and Canada Mortgage and Housing Corporation.

“I have clients where they had quite literally created an agreement of areas of the house that were off limits – whatever they could to kind of just co-exist before they could come up with a strategy that was feasible,” said Toronto realtor Rina Isufaj.

For Ms. Trinh, lower rents made living on her own more feasible. In February,

after landing briefly with her parents, she signed a lease for a one-bedroom apartment downtown at a monthly cost of about $1,950, a few months after the breakup.

For those living together after calling it quits on their relationship, there’s still the question of “who pays for what while you’re in limbo,” Ms. Ricchio said. “When two people are living separate lives under one roof, the old ‘we just split everything’ breaks down.”

There are tax implications as well. “Anyone claiming to be separated but living together, needs to ensure that before changing their status with the CRA and applying for benefits that they meet the criteria … you have to be able to prove you live separate lives and have separated financially,“ Ms. Ricchio said. “I have seen many make this claim only to have to pay back these benefits, thousands of dollars.”

Some wrongly assume they can’t afford to live alone after breaking up, Ms. Ricchio said. “Have you actually run the numbers on leaving, or are you just assuming you can’t? A lot of people skip straight to ‘we can’t afford it’ without ever building the budget,” she said.

That means comparing expected income with realistic projected living expenses and cross-referencing that with multiple housing options, including going back to renting after owning a home.

“We automatically assume we have to own a home,” Ms. Ricchio said. “If you factor in taking your current equity and being able to invest it, you may find that your annualized costs drop significantly.”

This article was first reported by The Globe and Mail