Dow Jones Hits Record High as Nasdaq Slides Amid Persistent Selling in Chip and Semiconductor Stocks

The Canadian Vanguard Stock Market Report Thursday July 2, 2026 Edition

.

The Toronto Market

Thursday’s Toronto Market Index

The S&P/TSX Composite Index advanced 109.68 points, or 0.31%, to close at 34,966.67. Although the index finished in positive territory, it settled well below the day’s high. The TSX is now trading above its 25-day moving average and remains well above its 50-day and 200-day moving averages.

Building on Tuesday’s 0.10% gain, the TSX added another 109.68 points, or 0.31%, on Thursday. The index opened slightly above the previous session’s close and remained positive through midday. It briefly slipped into negative territory during the afternoon before buyers returned about two hours before the close, lifting the index back into positive territory and well above the previous closing level.

The TSX last closed above the psychological 35,000 level on June 22, when it finished at 35,002, narrowly holding above that milestone. Trading resumed on Thursday following Wednesday’s market closure in observance of the Canada Day public holiday.

Thursday’s TSX Market Statistics

Market breadth on the TSX remained positive, with advancing issues (advancers) outnumbering declining issues (decliners). There were 1,206 advancers and 1,095 decliners, resulting in an advancer-to-decliner ratio of 1.10:1, or approximately 11 advancers for every 10 decliners. An additional 127 issues closed unchanged.

The exchange recorded 186 new 52-week highs and 36 new 52-week lows, compared with 172 new 52-week highs and 48 new 52-week lows in Tuesday’s session.

Total trading volume on the TSX reached 551,392,574 shares, representing a 24% increase from the 443,961,274 shares traded on Tuesday.

Compared with Tuesday, there were approximately 10% more declining issues and slightly fewer advancing issues. Despite this, overall market breadth remained positive. Canadian markets were closed on Wednesday in observance of the Canada Day public holiday.

.

Thursday’s Toronto TSX Market Wrap-Up Report

The S&P/TSX Composite Index gained 109.68 points, or 0.31%, to close at 34,966.67, extending Tuesday’s 0.10% advance following Wednesday’s Canada Day market holiday. Although the index finished well below its intraday high, it remained in positive territory as buying interest strengthened during the final two hours of trading.

From a technical perspective, the TSX continues to trade above its 25-day moving average and remains comfortably above both its 50-day and 200-day moving averages, indicating that the intermediate- and long-term bullish trends remain intact. However, the index once again failed to reclaim the psychologically important 35,000 level, suggesting that resistance near that mark remains significant.

Market breadth remained positive, with 1,206 advancing issues outnumbering 1,095 declining issues, producing an advancer-to-decliner ratio of 1.10:1. The TSX also recorded 186 new 52-week highs against 36 new lows, while trading volume increased 24% to 551.4 million shares, reflecting improved market participation following the holiday.

Mining companies dominated Thursday’s list of top-performing TSX stocks. Thomson Reuters Corporation was the session’s top-performing large-cap stock, while 13 of the top 15 gainers were mining companies from the Basic Materials sector, highlighting continued investor interest in resource stocks.

Sector performance was mixed, with five of the TSX’s ten major sectors finishing higher. Information Technology led the market with a 3.58% gain, followed by Basic Materials (+2.12%), Healthcare (+1.02%), Energy (+0.17%), and Industrials (+0.03%). On the downside, Financials declined 0.33%, while Consumer Discretionary was the weakest-performing sector, falling 1.45%.

Financial stocks weighed on the broader market despite the positive index close. All six of Canada’s largest banks finished lower, with Toronto-Dominion Bank leading the declines, down 1.84%. Bank of Nova Scotia lost 1.74%, while Bank of Montreal fell 1.49%. Manulife Financial Corp. was a notable exception within the Financials sector, rising 1.55%.

Among individual companies, Shopify Inc. outperformed after reports that Open Standard, an independent consortium backed by more than 140 companies, launched Open USD, a new U.S. dollar-backed stablecoin designed to facilitate global digital payments. Shopify is among the partners expected to integrate the stablecoin into its platform once it launches later this year, a development that investors viewed positively.

In contrast, Telesat Corporation surrendered much of Tuesday’s strong advance. After gaining 10.14% in the previous session, the stock fell 9.22% on Thursday, nearly erasing its earlier gains. Trading volume increased to approximately 57,400 shares, compared with 49,500 shares on Tuesday, indicating active profit-taking.

Small- and mid-cap stocks continued to attract investor attention. Notable performers included Aecon Group Inc. (ARE), which climbed 8.77% to close at $49.51 on 1.3 million shares traded, and SSR Mining Inc. (SSRM), which gained 8.28% to finish at $43.42 on 779,400 shares.

Key Takeaways for Traders and Investors

- The TSX extended its recent gains and continues to trade above all major moving averages, reinforcing the market’s underlying bullish technical structure.

- Resistance around the 35,000 level remains intact. A decisive close above this level could provide momentum for another leg higher.

- Strong market breadth, a sharp increase in trading volume, and a high number of new 52-week highs indicate that buying interest remains broad despite weakness in several large-cap financial stocks.

- Leadership continues to rotate toward Technology and Basic Materials, particularly mining stocks, while the Financials sector is showing signs of near-term weakness.

- Traders may continue to monitor relative strength in resource and technology shares while watching whether the banking sector stabilizes, as financial stocks remain a significant driver of the TSX’s overall direction.

.

The US Markets

Thursday’s U.S. Market Indexes

U.S. equity markets delivered a mixed performance on Thursday, with strength in blue-chip stocks offset by continued weakness in technology and semiconductor shares.

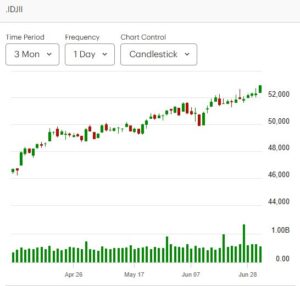

The Dow Jones Industrial Average advanced 594.83 points, or 1.14%, to close at 52,900.07, significantly outperforming the broader market. The S&P 500 was essentially unchanged, edging up just 0.01 point to finish at 7,483.24. Meanwhile, the Nasdaq Composite fell 207.36 points, or 0.80%, to close at 25,832.67, while the Russell 2000 Index declined 16.48 points, or 0.55%, ending the session at 2,996.11.

Thursday’s trading reflected a clear divergence between large-cap industrial stocks and the technology sector. While the Dow posted a strong gain of more than 1%, the Nasdaq remained under pressure as investors continued to reduce exposure to semiconductor and chip-related stocks. The ongoing selling in the semiconductor industry, which began in the previous session, accelerated on Thursday and was the primary factor weighing on the technology-heavy Nasdaq.

The Nasdaq’s decline pushed the index below the 26,000 level by the close. From a technical standpoint, the index is now trading below both its 25-day and 50-day moving averages, indicating weakening short- to intermediate-term momentum. Unless buying interest returns to the technology sector, the Nasdaq may remain vulnerable to additional downside pressure in the near term.

The flat performance of the S&P 500 highlights the market’s internal rotation, with gains in defensive and industrial names largely offsetting weakness in growth-oriented technology stocks. Investors continue to monitor whether the recent rotation away from high-growth sectors and toward more value-oriented and cyclical stocks will persist.

Key Takeaways for Traders and Investors

- The Dow’s strong advance contrasted sharply with the weakness in the Nasdaq, signaling continued sector rotation rather than broad market strength.

- Persistent selling in semiconductor and chip stocks remains a key headwind for the technology sector and the Nasdaq.

- The Nasdaq’s close below both its 25-day and 50-day moving averages weakens its near-term technical outlook.

- The S&P 500’s flat close suggests the broader market remains resilient despite significant weakness in technology, supported by gains in other sectors.

- Traders should monitor whether semiconductor stocks begin to stabilize, as a recovery in the group would likely be necessary for the Nasdaq to regain upward momentum.

Thursday’s U.S. Market Statistics

New York Stock Exchange (NYSE): Market breadth on the New York Stock Exchange (NYSE) remained firmly positive, with advancing issues comfortably outnumbering declining issues. The exchange recorded 2,633 advancing stocks, 1,857 declining stocks, and 504 unchanged issues, resulting in an advancer-to-decliner ratio of approximately 1.42:1, or roughly three advancing stocks for every two decliners.

The NYSE recorded 318 new 52-week highs and 111 new 52-week lows, compared with 353 new highs and 127 new lows in the previous session. Although the number of new highs declined by approximately 10% from Wednesday, it continued to significantly exceed the number of new lows, reflecting a healthy underlying market.

Total NYSE trading volume reached 5.57 billion shares, down 6% from 5.90 billion shares traded in the previous session. While trading activity eased modestly, the positive market breadth suggests buying interest remained broad across many sectors despite lighter volume.

NASDAQ: Market internals on the NASDAQ weakened as declining stocks narrowly outnumbered advancing stocks. The exchange reported 2,548 declining issues, 2,419 advancing issues, and 346 unchanged issues, resulting in a decliner-to-advancer ratio of approximately 1.05:1. Although the margin was relatively small, the negative breadth marked a deterioration in overall market participation.

NASDAQ recorded 321 new 52-week highs and 106 new 52-week lows, compared with 350 new highs and 96 new lows in the previous session. The decline in new highs, coupled with a slight increase in new lows, reflects moderating market momentum, particularly within growth-oriented sectors.

Trading volume on the NASDAQ totaled 9.93 billion shares, representing a 4.5% increase from the 9.49 billion shares traded in the previous session. Despite the increase, overall volume remained slightly below the exchange’s 50-day average daily trading volume.

The deterioration in NASDAQ market breadth coincided with another day of weakness in artificial intelligence, semiconductor, and chip-related stocks. Selling pressure in these high-growth sectors weighed heavily on the technology-heavy Nasdaq Composite, which finished below both its 25-day and 50-day moving averages, reinforcing the recent weakening in its short- and intermediate-term technical outlook.

Key Takeaways for Traders and Investors

- NYSE market breadth remained constructive, with advancers significantly outnumbering decliners and new 52-week highs continuing to exceed new lows by a wide margin.

- NASDAQ market breadth turned negative, reflecting growing weakness in technology and growth stocks despite relatively balanced advancing and declining issues.

- Increased NASDAQ trading volume alongside falling technology shares suggests institutional participation in the recent selling, particularly within semiconductor and AI-related companies.

- The Nasdaq Composite’s close below both its 25-day and 50-day moving averages weakens its technical picture and could encourage additional short-term selling if support levels fail to hold.

- Traders should exercise increased risk management when trading semiconductor, AI, and chip stocks until signs of stabilization or renewed buying emerge. At the same time, investors may wish to monitor whether market leadership continues to rotate toward industrial, financial, and other value-oriented sectors while technology consolidates.

Thursday’s U.S. Market Wrap-Up Report

U.S. equity markets finished Thursday on a mixed note, with a sharp divergence between the blue-chip Dow Jones Industrial Average and the technology-heavy Nasdaq Composite. The Dow Jones Industrial Average surged 594.83 points, or 1.14%, to a record closing high of 52,900.07, while the S&P 500 finished virtually unchanged. In contrast, the Nasdaq Composite fell 0.80%, weighed down by another broad-based sell-off in semiconductor and artificial intelligence (AI) stocks. The Russell 2000 Index also ended lower, declining 0.55%.

The market’s performance reflected an ongoing rotation out of high-growth technology shares and into more defensive and value-oriented sectors. While profit-taking has likely contributed to the recent weakness in semiconductor stocks—many of which have posted substantial gains since the beginning of the year—the intensity and breadth of the selling suggest investors are reassessing valuations across the AI and semiconductor space.

From a technical perspective, the Nasdaq Composite closed below both its 25-day and 50-day moving averages, signaling weakening short- and intermediate-term momentum. Meanwhile, the Dow continues to display relative strength, underscoring the divergence in market leadership.

Despite the Nasdaq’s weakness, overall market participation remained constructive on the New York Stock Exchange (NYSE). Advancing stocks outnumbered declining stocks by approximately 1.42 to 1, while the exchange recorded 318 new 52-week highs versus 111 new lows. On the NASDAQ, however, market breadth turned slightly negative as decliners narrowly exceeded advancers, reflecting the continued pressure on growth and technology shares. Trading volume on the NASDAQ increased 4.5%, suggesting elevated institutional activity during the technology sell-off.

Eight of the ten major U.S. market sectors finished higher. Healthcare led the market with a 2.80% gain, followed by Consumer Durables & Services (+2.20%), Basic Materials (+1.77%), Utilities (+1.54%), Energy (+1.15%), and Financials (+0.73%). Technology was the weakest-performing sector, declining 1.44%, as semiconductor and AI-related stocks remained under heavy selling pressure.

Semiconductor and Technology Stocks Remain Under Pressure

The semiconductor sector experienced another difficult session, with selling extending for a second consecutive day. Several industry leaders recorded substantial losses:

- Sandisk Corporation declined 14.13% on 17.3 million shares traded and has now fallen more than 21% over the past two sessions.

- Marvell Technology (MRVL) dropped 9.80% on 38.6 million shares.

- Tower Semiconductor Ltd. (TSEM) lost 10.76% on 2.7 million shares.

- Micron Technology fell 5.49% on 61.8 million shares.

- Intel Corporation (INTC) declined 5.25% on 124.9 million shares.

- Advanced Micro Devices (AMD) lost 4.26%.

The widespread nature of the declines illustrates that selling pressure was not confined to a handful of companies. Instead, investors broadly reduced exposure across semiconductor, chip manufacturing, AI infrastructure, and related technology industries.

Weakness also spread beyond chipmakers. Dell Technologies, a major AI server infrastructure provider, fell 7.30% on 6.6 million shares traded, while Celestica Inc. declined 6.97%. In contrast, Shopify Inc. bucked the broader technology trend, gaining 4.55%.

Large-cap technology stocks also came under pressure, with Tesla and Meta Platforms among the notable contributors to Thursday’s weakness in the Nasdaq.

Key Takeaways for Traders and Investors

- The market continues to exhibit clear sector rotation, with capital flowing into healthcare, industrial, financial, utility, and other defensive sectors while technology and semiconductor stocks remain under pressure.

- The Dow Jones continues to demonstrate relative strength, reaching another record closing high, while the Nasdaq has entered a period of technical weakness after falling below both its 25-day and 50-day moving averages.

- Although the recent decline in semiconductor stocks is likely being driven in part by profit-taking following exceptional gains earlier this year, the elevated trading volumes suggest institutional investors are actively reducing exposure across the sector.

- NYSE market breadth remains healthy, indicating that weakness is concentrated in technology rather than reflecting broad-based market deterioration.

- Until semiconductor and AI-related stocks establish a technical base and buying volume returns, traders should expect above-average volatility in these sectors and employ disciplined risk management. Investors may continue to monitor whether the current rotation into value-oriented and defensive sectors has further room to run while awaiting signs of stabilization in technology.

.

NOTICE TO READERS

The Canadian Vanguard Stock Market is about empowering you to build and manage your wealth by yourself. There is certainly no magic in managing finances or wealth but one needs to know what to do and commit to doing what is needed. When you are ready to start the journey to Take Charge and Put Your Destiny In Your Own Hands, read The Canadian Vanguard every market day. If you need more related information, Contact Us

Our readers are strongly advised to conduct their own research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is no guarantee of future price appreciation. Any recommendation is not a guarantee of any particular stock’s future prices, and The Canadian Vanguard accepts no responsibility or liability for investors’ or readers’ purchases.

Stocks In The News/ Stocks To Watch and Market Strategy will soon be available only to Paying Subscribers. The dollar sign “$” in the Toronto Market section in the articles only stands for Canadian dollar and in the US market section “$” stands for US dollar.

(c) This article is published by The Canadian Vanguard on July 2, 2026