Equity Markets Sell Off as Geopolitical Risks Drive Elevated Uncertainty

The Canadian Vanguard Stock Market Report – Wednesday March 25, 2026 Edition.

.

The Toronto Market

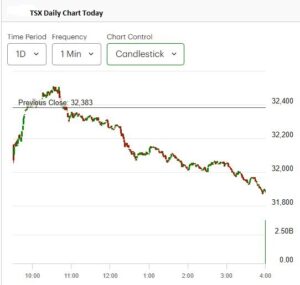

The Toronto Market Index

The Toronto S&P/TSX Composite Index fell sharply, dropping 495.08 points (-1.53%) to close at 31,887.52. A consistent pattern emerged across major North American market indexes throughout the trading day. Markets opened lower than the previous session’s close, rallied within the first hour to briefly move above prior closing levels, and then steadily declined for the remainder of the day, finishing near their lows.

Investor sentiment was driven by a single dominant factor: geopolitical tensions. Specifically, an ultimatum issued to Iran by the U.S. President weighed heavily on markets. As a result, trading activity was influenced less by company fundamentals, earnings performance, or long-term business outlooks, and more by concerns surrounding potential conflict.

![]()

Today’s TSX Market Statistics

On the TSX, declining issues significantly outnumbered advancing issues. A total of 1,787 stocks declined, while 403 advanced, resulting in a decliner-to-advancer ratio of 4.43 to 1—approximately nine decliners for every two advancers. Additionally, 84 issues remained unchanged.

The exchange recorded 61 new 52-week highs and 55 new 52-week lows, compared to 36 new highs and 22 new lows in the previous session.

Total trading volume on the TSX reached 483,253,342 shares, representing a 5% decrease from the 507,199,828 shares traded yesterday.

Today’s Toronto Market Wrap-Up Report

The TSX Composite Index declined 1.53% today, reflecting a market environment largely disconnected from underlying business fundamentals. Instead, price action was overwhelmingly driven by geopolitical risk—specifically escalating tensions between the United States and Iran. While Canada is not directly involved, the high correlation between Canadian and U.S. equity markets means that external shocks of this magnitude tend to transmit quickly into the TSX.

From a market structure perspective, today’s session followed a classic risk-off pattern: an initial attempt to recover early losses was met with sustained selling pressure throughout the day. This suggests institutional repositioning rather than retail-driven volatility, with capital rotating away from cyclical and growth-sensitive sectors.

Sector performance reinforced this defensive shift. Utilities was the only sector to finish in positive territory, gaining 0.28%, underscoring its role as a traditional safe haven during periods of uncertainty. Energy (-0.16%) and Telecommunications Services (-0.25%) showed relative resilience, likely supported by stable cash flows and, in the case of Energy, sensitivity to potential supply disruptions. In contrast, economically sensitive sectors saw pronounced weakness. Financials declined 1.28% and Technology fell 1.56%, while Consumer Discretionary and Basic Materials led the downturn, each dropping 3.89%, highlighting a broad-based risk aversion trade.

The Canadian banking sector—often viewed as a proxy for domestic economic confidence—came under notable pressure. Bank of Montreal declined 3.12%, making it the weakest among the Big Six. Canadian Imperial Bank of Commerce fell 2.84%, while the remaining major banks posted losses in the range of 1.1% to 1.6%. This collective weakness signals investor concern around macroeconomic stability and credit conditions in a heightened-risk environment.

For traders and short-term investors, the current market regime demands caution. While “buying the dip” can be profitable in fundamentally driven pullbacks, today’s decline is event-driven and highly sensitive to headline risk. Market direction in the near term will likely hinge on geopolitical developments rather than earnings or economic data. This creates a binary setup: de-escalation headlines could trigger sharp relief rallies, while further escalation may lead to accelerated downside.

Selective strength emerged in names with direct or indirect exposure to geopolitical dynamics. Suncor Energy Inc. gained 0.72%, benefiting from energy market sensitivity to supply risks. Thomson Reuters Corporation rose 3.71%, reflecting demand for information and analytics during uncertain periods. Ovintiv Inc. advanced 2.2%, while Methanex Corporation added 1.89%, both supported by commodity-linked tailwinds. Bird Construction Inc. gained 2.71%, showing resilience despite broader cyclical weakness.

Investor and Traders Take Away

Traders should be mindful that in news-driven markets, price momentum can reverse abruptly. Elevated volatility compresses time horizons and reduces the reliability of traditional valuation metrics. Risk management, position sizing, and disciplined entry/exit strategies become critical.

In summary, the TSX is currently trading as a macro-sensitive, headline-driven market. Until geopolitical clarity improves, investors should expect continued volatility, sector rotation into defensives, and heightened correlation with U.S. market movements.

.

The US Markets

U.S. Market Indexes

U.S. equities extended their sell-off, reversing the prior session’s attempted stabilization and accelerating to the downside. The Dow Jones Industrial Average fell 469.38 points (-1.01%) to close at 45,960.11. The S&P 500 declined 114.74 points (-1.74%) to 6,477.16, while the Nasdaq Composite led losses, dropping 521.74 points (-2.38%) to 21,408.08. The Russell 2000 shed 43.06 points (-1.70%) to finish at 2,493.32.

Despite the broad-based decline, intraday price action followed a uniform pattern across all major indexes: a weaker open, an early-session rebound that briefly tested prior closing levels, and a sustained sell-off into the close. This synchronized behavior suggests macro-driven, systematic selling rather than idiosyncratic or sector-specific weakness.

From a market dynamics standpoint, today’s session was dominated by geopolitical risk tied to escalating tensions between the U.S. and Iran. As a result, traditional drivers such as earnings expectations, economic data, and company fundamentals were largely sidelined. Correlation across asset classes and sectors increased, a typical hallmark of risk-off environments.

Performance dispersion across indexes highlights risk sensitivity. The Dow Jones Industrial Average, with its heavier weighting in defensive and value-oriented names, showed relative resilience with a 1.01% decline. In contrast, the Nasdaq Composite’s 2.38% drop underscores the vulnerability of growth and technology stocks to risk repricing, particularly as investors de-risk high-multiple exposures. The S&P 500 and Russell 2000 declines further confirm broad participation in the sell-off, spanning both large-cap and small-cap segments.

For traders, the key takeaway is that the market is currently operating in a headline-driven regime with elevated volatility and reduced predictability. The failed intraday rallies point to weak dip-buying conviction and suggest that downside momentum may persist in the absence of stabilizing news flow.

In this environment, capital preservation becomes a priority. Tactical positioning, tighter risk controls, and an awareness of overnight headline risk are essential, as sentiment can shift rapidly with geopolitical developments.

U.S. Market Breadth and Volume Analysis

Market internals on both the New York Stock Exchange and the NASDAQ confirmed the strength and breadth of today’s sell-off, reinforcing the risk-off tone observed across major indexes.

On the NYSE, declining issues significantly outpaced advancers, with 3,455 decliners versus 1,085 advancers and 333 unchanged stocks. This produced a decliner-to-advancer ratio of 3.18 to 1, indicating broad-based selling pressure across sectors rather than isolated weakness.

New 52-week highs totaled 115, while new lows reached 127. Although both figures declined from the previous session (149 highs and 199 lows), the fact that new lows continued to exceed new highs signals persistent downside pressure and limited bullish momentum.

Total NYSE trading volume came in at approximately 4.93 billion shares, down 9% from the previous session. This decline in volume alongside falling prices may suggest a lack of aggressive panic selling, but it also reflects reduced conviction among buyers stepping in to absorb supply.

On the NASDAQ, market breadth was similarly negative, with 3,423 decliners compared to 1,385 advancers and 314 unchanged issues. The resulting decliner-to-advancer ratio of 2.47 to 1 (roughly five decliners for every two advancers) highlights sustained weakness, particularly within growth and technology segments.

Notably, NASDAQ new lows expanded sharply to 328, up from 203 in the prior session, while new highs remained relatively flat at 81. This divergence—stable highs but rising lows—is a bearish signal, pointing to increasing downside momentum and deterioration in market leadership.

NASDAQ trading volume totaled approximately 7.99 billion shares, down 4% from the previous session. Similar to the NYSE, the lighter volume suggests a controlled sell-off rather than capitulation, but also indicates limited buying interest at current levels.

Key Takeaway for Traders and Investors:

Market breadth and volume metrics confirm that today’s decline was both broad and structurally weak. The expansion in new lows—particularly on the NASDAQ—combined with weak advance-decline ratios suggests that downside risks remain elevated. Until breadth stabilizes and new highs begin to expand meaningfully, rallies are likely to face resistance and may prove short-lived.

Today’s U.S. Market Wrap-Up Report

U.S. equities experienced a broad and decisive sell-off, with all major indexes closing significantly lower. The Nasdaq Composite led the decline, falling approximately 2.8%—a move that signals meaningful risk repricing rather than routine volatility. While a 1% daily decline in a major index is typically viewed as notable weakness, drawdowns exceeding 2% often indicate a shift in market regime, warranting closer scrutiny of macro conditions and portfolio risk exposure.

At present, the market is operating in a predominantly news-driven environment, with geopolitical developments—particularly escalating tensions involving the United States and Iran—overshadowing traditional fundamentals. In such conditions, price discovery becomes increasingly erratic, correlations rise, and the predictive value of technical and fundamental analysis diminishes. This type of regime is often characterized by sharp reversals and elevated headline risk, making short-term market direction difficult to anticipate.

From a risk management perspective, a more defensive posture is warranted. Elevated cash positions and reduced exposure can help preserve capital during periods of heightened uncertainty. For many investors, limiting equity exposure and prioritizing liquidity until volatility subsides may be a prudent approach.

Sector performance reflected a clear defensive rotation. Energy was the only sector to finish in positive territory, gaining 1.19%, supported by sensitivity to potential supply disruptions. Telecommunications Services (-0.34%) and Healthcare (-0.44%) showed relative resilience, consistent with their defensive characteristics. In contrast, cyclicals and growth-oriented sectors bore the brunt of the selling pressure. Industrials declined 2.18%, while Technology dropped sharply by 3.07%, making it the weakest-performing sector. Financials (-1.17%) and Basic Materials (-1.91%) also posted notable losses.

In company-specific developments, semiconductor and storage names came under significant pressure, highlighting the vulnerability of high-beta technology stocks in risk-off environments. Micron Technology Inc. declined 6.97%, continuing its pullback from earlier highs and trading below key short-term moving averages. From a technical standpoint, a break below the 50-day moving average often signals weakening momentum and increased downside risk.

SanDisk Corporation fell 11%, reflecting aggressive de-risking despite still trading above longer-term technical support levels. Western Digital dropped 7.69%, while Seagate Technology Holdings declined 8.33%, underscoring broad-based weakness across the storage segment.

Key Takeaway:

Markets are currently in a high-volatility, headline-driven phase where capital preservation should take precedence over return maximization. Until geopolitical risks subside and market internals stabilize, traders should expect continued sharp swings, reduced reliability of technical signals, and heightened downside risk—particularly in high-growth and momentum-driven sectors.

NOTICE TO READERS

The Canadian Vanguard Stock Market is about empowering you to build and manage your wealth by yourself. There is certainly no magic in managing finances or wealth but one needs to know what to do and commit to doing what is needed. When you are ready to start the journey to Put Your Destiny In Your Own Hands, read The Canadian Vanguard every market day. If you need more information please Contact Us

Our readers are strongly advised to conduct their own research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is no guarantee of future price appreciation. Any recommendation is not a guarantee of any particular stock’s future prices, and The Canadian Vanguard accepts no responsibility or liability for investors’ or readers’ purchases.

Stocks In The News/ Stocks To Watch and Market Strategy will soon be available but only to Paying Subscribers. The dollar sign “$” in the Toronto Market section in the articles only stands for Canadian dollar and in the US market section “$” stands for US dollar.

(c) This article is published by The Canadian Vanguard on March 26, 2026