Risk-Off Sentiment Triggers Broad Sell-Off and Heightened Volatility

The Canadian Vanguard Stock Market Report – Thursday February 12, 2026 Edition.

.

The Toronto Market

The S&P/TSX Composite Index fell 788.91 points, or 2.37%, closing at 32,465.28. The benchmark index for the Toronto market declined from the opening bell and failed to gain the momentum needed to recover into positive territory. It was a notably negative session, as the index erased the combined gains of the previous three trading days in a single day.

Thursday’s TSX Market Statistics

On the TSX, declining issues outnumbered advancing issues. There were 1,542 decliners compared with 673 advancers, while 117 issues remained unchanged. This results in a decliner-to-advancer ratio of approximately 2.29 to 1.

There were 256 new 52-week highs and 64 new 52-week lows, compared with 282 new highs and 14 new lows recorded in the previous session.

Total trading volume on the TSX reached 573,796,143 shares, up 30% from the 442,273,319 shares traded on Tuesday. We did not publish a report yesterday due to circumstances beyond our control.

.

The US Markets

U.S. Market Indexes

The market closed broadly lower, with all major indexes finishing in negative territory. The Dow Jones Industrial Average fell 669.42 points, or 1.34%, to close at 49,451.98. The S&P 500 declined 108.71 points, or 1.57%, ending the session at 6,832.76. The Nasdaq Composite dropped 469.32 points, or 2.03%, to finish at 22,597.15.

The Russell 2000 Index lost 53.64 points, or 2.01%, closing at 2,615.83. The small-cap index struggled throughout the session, declining sharply from the opening bell and remaining under pressure through the close. Small-cap stocks broadly underperformed.

Both the Dow Jones Industrial Average and the S&P 500 closed at their session lows, while the Nasdaq Composite and Russell 2000 finished slightly above their lowest levels of the day.

Thursday’s U.S. Market Statistics

New York Stock Exchange (NYSE): Declining issues outnumbered advancing issues. There were 1,900 decliners, 852 advancers, and 87 issues unchanged, resulting in a decliner-to-advancer ratio of 2.23 to 1 — roughly two decliners for every advancer.

The exchange recorded 370 new 52-week highs and 134 new 52-week lows, compared with 309 new highs and 38 new lows in the previous session.

Total NYSE trading volume reached 7,226,032,358 shares, approximately 25% higher than the 5,737,836,060 shares traded on Tuesday.

NASDAQ: On the NASDAQ, declining stocks also outnumbered advancing stocks. There were 3,581 decliners and 1,305 advancers, with 284 issues unchanged, producing a decliner-to-advancer ratio of 2.74 to 1 — nearly three decliners for every advancer.

The exchange posted 324 new 52-week highs and 385 new 52-week lows, compared with 313 new highs and 123 new lows recorded on Tuesday.

Total NASDAQ trading volume amounted to 9,118,779,442 shares, approximately 3% higher than the previous session’s volume of 8,865,894,465 shares.

U.S. Market Wrap-Up Report

Thursday’s session was marked by broad-based selling pressure that erased the gains from the market’s prior three-day advance. All major indexes closed decisively lower, with the Dow Jones Industrial Average down 1.34%, the S&P 500 off 1.57%, the Nasdaq Composite falling 2.03%, and the Russell 2000 declining 2.01%. Notably, both the Dow and the S&P 500 finished at their intraday lows — a sign that sellers remained firmly in control through the closing bell.

Market breadth confirmed the weakness. On the NYSE, decliners outpaced advancers by more than 2-to-1, while the NASDAQ registered nearly three decliners for every advancer. New 52-week lows expanded meaningfully on both exchanges compared with the previous session, particularly on the NASDAQ where new lows outnumbered new highs. Volume rose sharply on the NYSE (up 25%) and increased modestly on the NASDAQ, suggesting institutional participation in the sell-off rather than light, retail-driven trading.

Sector performance reflected a classic risk-off rotation. Basic Materials led the decline, dropping 2.99% , while Technology fell 2.46%. The Nasdaq’s sharper pullback relative to the Dow underscores continued pressure in growth and momentum names. In contrast, Telecommunications Services, Durable Consumer Goods & Services, and Utilities outperformed on a relative basis. Defensive positioning in Utilities and Telecommunications indicates capital rotation toward perceived stability amid heightened volatility.

Within Technology, investor reaction to earnings drove significant single-stock volatility. Applovin (APP) plunged 20% despite beating estimates, reflecting how elevated expectations can amplify downside reactions. Cisco Systems (CSCO) fell 12% following earnings, with concerns centered on competitive and AI-related disruption risks. These moves reinforce the market’s current intolerance for uncertainty in large-cap tech.

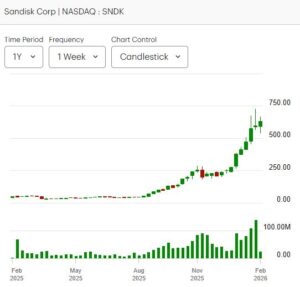

However, performance within the broader technology ecosystem was not uniform. Disk drive manufacturers outperformed, with SanDisk up 5.6%, Seagate gaining 5.8%, and Western Digital rising 3.8%. The strength in storage names highlights continued structural demand tied to data center expansion and AI infrastructure build-out.

Micron Technology (MU) also finished modestly higher, though it retreated from stronger intraday gains — a sign of profit-taking into broader market weakness.

Investor/Trader Takeaway

Thursday’s price action signals a clear shift toward caution in the near term. Expanding new lows, decisively negative breadth, and higher NYSE volume point to institutional distribution rather than routine profit-taking. The market’s intolerance for earnings-related uncertainty — particularly in high-valuation growth stocks — suggests that volatility may remain elevated.

For investors, this is a time to reassess risk exposure, especially in crowded technology trades where expectations remain high. Defensive sector rotation into Utilities and Telecommunications indicates a preference for stability, and portfolio balance should reflect that shift if market weakness persists.

For traders, the focus should be on breadth stabilization, volume patterns, and whether the major indexes can reclaim key support levels quickly. A failure to do so could invite additional downside momentum, while improving internals and leadership rotation would signal that this pullback is corrective rather than the start of a broader trend reversal.

Commodities and Bonds

Oil:

West Texas Intermediate (WTI) crude futures fell nearly 3% to $62.84 per barrel and are on track for a weekly decline as geopolitical tensions eased following U.S.–Iran talks. As of 12:30 a.m. EST Friday, U.S. crude was down $0.15 at $62.69 per barrel.

Gold and Silver:

Gold rose $243.50, or 0.50%, to $4,972.60 per troy ounce. Silver gained $0.40, or 0.53%, to $76.10 per ounce as of 12:30 a.m. EST Friday.

Bitcoin:

Bitcoin (BTC-USD), which traded higher earlier in the session, was up $574.78, or 0.88%, at $66,041.00 at the time of this update.

10-Year Treasury Yield:

The yield on the benchmark 10-year Treasury note declined seven basis points earlier in the day to 4.10%, following weaker housing data that showed the sharpest drop in home sales since 2022. As of 12:30 a.m. EST Friday, the 10-year yield stood at 4.113%.

After-Hours Action

U.S. equity futures moved lower Thursday evening into early Friday trading. As of 12:30 a.m. EST:

- Dow futures were down 139 points, or 0.28%, versus fair value.

- S&P 500 futures fell 21.50 points, or 0.31%, to 6,830.30.

- Nasdaq 100 futures declined 96.00 points, or 0.39%, to 24,663.75.

The pullback in futures suggests continued caution following Thursday’s broad market sell-off.

NOTICE TO READERS

The Canadian Vanguard Stock Market is about empowering you to build and manage wealth by yourself. There is certainly no magic in managing finances or wealth but one needs to know what to do and commit to doing what is needed. When you are ready to start the journey to Put Your Destiny In Your Own Hands, read The Canadian Vanguard every market day. If you need more information please Contact Us

Our readers are strongly advised to conduct their own research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is no guarantee of future price appreciation. Any recommendation is not a guarantee of any particular stock’s future prices, and The Canadian Vanguard accepts no responsibility or liability for investors’ or readers’ purchases.

Stocks In The News/ Stocks To Watch and Market Strategy will soon be available but only to Paying Subscribers.

(c) This article is published by The Canadian Vanguard on February 12, 2026