The Canadian Vanguard Stock Market Report Weekend May 15-17, 2026 Edition

Markets Slide Sharply as Investors React to Disappointing Outcome from Trump’s China Visit

.

The Toronto Market

Friday’s Toronto Market Index

The Toronto S&P/TSX Composite Index fell 434.92 points, or 1.27%, to close at 33,833.35 on Friday. The decline was more than double the loss recorded in the previous session, reflecting a notably weak trading day for Canadian equities. Trading volume was significantly higher than the prior session, indicating increased selling pressure. The TSX remains in pullback territory as market sentiment continues to weaken.

Friday’s TSX Market Statistics

On the TSX, declining issues significantly outnumbered advancing issues. There were 1,715 decliners compared with 519 advancers, resulting in a decliner-to-advancer ratio of 3.30-to-1 — or roughly three declining stocks for every advancing stock. Meanwhile, 98 issues closed unchanged.

The exchange recorded 120 new 52-week highs and 84 new 52-week lows, compared with Thursday’s totals of 380 new highs and 48 new lows, reflecting a notable deterioration in market momentum.

Total trading volume on the TSX reached 562,564,641 shares, representing a 25% increase from the 448,724,120 shares traded on Thursday. The significantly higher trading activity, combined with sharply negative market breadth, suggests intensified selling pressure during the session.

Today’s market weakness was influenced in part by developments surrounding the meeting in China involving President Trump and the Chinese President, which weighed on investor sentiment.

Friday’s Toronto Market Wrap-Up Report

The Toronto market ended sharply lower on Friday as risk sentiment deteriorated across most sectors. Only three sectors closed in positive territory, with Technology leading the market for a second consecutive session, gaining 2.70%. Energy followed with a 1.15% advance, while Telecommunications Services posted a modest 0.10% gain. Financials slipped 0.47%, while Basic Materials was the clear laggard, plunging 5.75% and extending its weakness for a second straight session.

Friday’s selloff effectively reversed Thursday’s rebound and reinforced the market’s recent pattern of heightened volatility. After a weak Wednesday, a strong Thursday recovery, and another sharp decline Friday, investors are now facing a market that is reacting aggressively to geopolitical headlines and macroeconomic uncertainty. Much of the volatility continues to be tied to developments surrounding President Trump’s visit to China and ongoing negotiations between the world’s two largest economies. Traders should expect elevated headline risk and potentially rapid sector rotation in the near term.

Weekly Market Performance: Despite Friday’s sharp weakness, several sectors still finished the week with respectable gains. Energy led the TSX higher this week, advancing 4.85%, supported by stronger commodity pricing and continued investor interest in traditional energy producers. Basic Materials gained 4.67% for the week despite Friday’s steep decline, highlighting how quickly sentiment can shift in highly cyclical sectors.

Technology, however, remained under pressure on a weekly basis, falling 8.04% despite back-to-back daily leadership performances. This divergence suggests that traders may be selectively buying oversold technology names rather than initiating broad-based long-term positioning. Telecommunications Services and Financials posted modest weekly gains of 0.82% and 0.80%, respectively, while retail-oriented sectors continued to underperform amid concerns over consumer spending and economic growth.

Investor and Trader Outlook

For investors, the current environment continues to favour selective positioning rather than aggressive market-wide exposure. Defensive sectors and cash-generating companies remain relatively attractive as volatility increases. Long-term investors should continue focusing on balance-sheet strength, recurring revenue growth, and companies benefiting from structural themes such as artificial intelligence infrastructure, energy demand, and digital transformation.

For short-term traders, volatility is creating opportunity, particularly in sectors experiencing strong momentum shifts. However, disciplined risk management remains essential as market direction is being heavily influenced by geopolitical developments rather than traditional valuation metrics or earnings trends. Traders should monitor volume trends closely, as elevated volume during down sessions often signals institutional selling pressure.

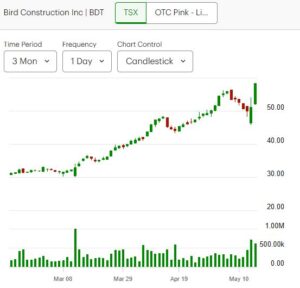

Stock in Focus: Bird Construction Inc. (BDT): Bird Construction Inc. (BDT) emerged as one of Friday’s strongest performers, surging 14.2% to close at $58.35 on volume of 621,900 shares. Investor enthusiasm was driven by the company’s expanding relationship with Bell Canada and Bell’s ambitious AI infrastructure expansion plans.

Bell Canada’s proposed 800MW data center initiative represents a potentially significant long-term catalyst for Bird Construction. The growing demand for AI computing infrastructure and large-scale data centers continues to create major opportunities for engineering, construction, and infrastructure firms. The data center buildout theme remains one of the strongest long-term investment trends tied to artificial intelligence growth.

Energy Transition Sentiment Shifting:

Investor sentiment within the energy sector also appears to be evolving. Nuclear-related suppliers weakened notably Friday, while energy storage and infrastructure-related companies attracted stronger interest. Cameco Corp. declined 4.46% on volume of 3.1 million shares, reflecting profit-taking and broader weakness in uranium-linked equities.

The market appears to be reassessing how capital will flow within the broader energy transition theme. While nuclear energy remains strategically important, investors are increasingly focusing on grid modernization, battery storage, and AI-driven electricity demand growth.

Shopify Attempts Stabilization: Shopify Inc. gained 3.18% Friday despite the broader market weakness, suggesting renewed speculative interest in large-cap Canadian technology stocks. However, the stock remains below its 200-day moving average, which continues to signal technical weakness from a longer-term trading perspective.

For traders, Shopify may offer short-term momentum opportunities if buying strength continues. Longer-term investors, however, may prefer to wait for a confirmed technical breakout above major resistance levels before increasing exposure.

Precious Metals Sector Under Pressure: Gold and silver mining stocks remained under heavy pressure Friday as investors rotated away from defensive commodity positions. Agnico Eagle Mines Ltd. declined 6.22% on volume of 1.2 million shares, while Wheaton Precious Metals Corp. fell 6.10% with approximately 700,000 shares traded.

The precious metals sector may require a stabilization period before regaining momentum. Traders should watch gold price action, bond yields, and U.S. dollar strength closely, as these factors are likely to determine near-term direction for mining equities. Long-term investors may eventually find value opportunities emerging if weakness persists and commodity fundamentals stabilize.

.

The US Markets

Friday’s U.S. Market Indexes

U.S. equity markets closed sharply lower on Friday as investors shifted toward a more risk-off posture amid geopolitical uncertainty and profit-taking in extended growth sectors. All four major indexes finished the session deep in negative territory, with small-cap stocks experiencing the heaviest selling pressure.

The Dow Jones Industrial Average dropped 537.29 points, or 1.07%, to close at 49,526.29. The S&P 500 declined 92.74 points, or 1.24%, ending the session at 7,408.50, while the Nasdaq Composite fell 410.08 points, or 1.54%, to finish at 26,225.14. The Russell 2000 Index, which tracks smaller-cap companies, plunged 69.79 points, or 2.44%, to close at 2,793.30.

From a technical standpoint, Friday’s session carried several important signals for investors and traders. The Dow Jones Industrial Average fell back below the psychologically significant 50,000 level only one day after closing above it for the first time on Thursday. That failed breakout now potentially transforms the 50,000 mark into a near-term resistance level that traders will monitor closely in upcoming sessions.

The S&P 500 and Nasdaq Composite also retreated sharply, although both indexes remain near historically elevated levels. Prior to Friday’s decline, both indexes had become technically extended following strong rallies driven largely by artificial intelligence, mega-cap technology, and momentum-driven buying. Friday’s pullback may therefore represent a healthy near-term correction rather than the beginning of a broader market breakdown — provided support levels hold in the coming sessions.

The most concerning development Friday came from the Russell 2000 and the broader small-cap space. Small-cap stocks were heavily sold, reflecting growing investor caution toward economically sensitive and higher-risk equities. When an index declines 2% or more in a single session, especially on broad participation and elevated volume, traders typically watch carefully for confirmation of either stabilization or further downside over the next one to two sessions.

Investor sentiment was negatively impacted in part by perceptions that President Trump’s visit to China, accompanied by several high-profile corporate executives, produced limited immediate economic or trade breakthroughs. Markets had likely priced in stronger progress, leaving investors disappointed by the lack of substantive developments.

Investor and Trader Outlook

For investors, Friday’s market action reinforces the importance of portfolio discipline in an environment increasingly driven by geopolitical headlines and valuation concerns. Markets remain near elevated levels despite signs of slowing momentum beneath the surface. Defensive positioning, balanced sector exposure, and careful attention to earnings quality may become increasingly important if volatility persists.

For traders, Friday’s selloff may create both risk and opportunity. Technology and momentum stocks remain vulnerable to additional profit-taking after extended rallies, while small-cap weakness suggests risk appetite is fading. Traders should closely monitor whether major indexes stabilize near key technical support levels early next week. A quick rebound could indicate the pullback was largely technical in nature, while continued weakness may signal a broader corrective phase developing across U.S. equities.

Market participants should also pay close attention to bond yields, U.S.-China developments, and institutional trading volume, as these factors are likely to drive near-term market direction.