Semiconductor Sell-Off Weighs on Nasdaq as Broader Market Holds Firm

The Canadian Vanguard Stock Market Report Wednesday July 1, 2026 Edition

.

The Toronto Market

Canadian markets were closed on July 1 for Canada Day Public Holiday. Market will reopen as usual on Thursday, July 2.

.

US Markets will close on Friday, July 3 in lieu of July 4 being on a Saturday.

.

The US Markets

Wednesday’s U.S. Market Indexes

The Dow Jones Industrial Average slipped 13.96 points (-0.03%) to close at 52,305.24. The S&P 500 declined 16.13 points (-0.22%) to finish at 7,483.23. The Nasdaq Composite fell 173.69 points (-0.66%) to 26,040.03, while the Russell 2000 Index lost 11.78 points (-0.39%) to close at 3,012.59.

Wednesday’s trading session ended lower across all major U.S. equity indexes, including small-cap stocks, although losses in the Dow Jones Industrial Average were modest. Overall market weakness was relatively contained, with the technology sector—particularly chip and semiconductor stocks—experiencing the steepest declines. The sell-off in semiconductor shares weighed heavily on the Nasdaq, although the index remained above the 26,000 level.

From a technical perspective, the Nasdaq is trading near its 25-day moving average while remaining comfortably above both its 50-day and 200-day moving averages, indicating that its longer-term uptrend remains intact. Similarly, the S&P 500 continues to trade well above its 25-day, 50-day, and 200-day moving averages, reflecting continued underlying technical strength despite the day’s pullback.

Wednesday’s U.S. Market Statistics

New York Stock Exchange (NYSE): Advancing issues outnumbered declining issues during Wednesday’s trading session. Specifically, there were 2,403 advancers, 2,240 decliners, and 402 unchanged issues, resulting in an advancer-to-decliner ratio of approximately 1.07:1, indicating slightly positive market breadth.

The NYSE recorded 353 new 52-week highs and 127 new 52-week lows, compared with 349 new highs and 154 new lows on Tuesday. The increase in new highs and the decline in new lows suggest that underlying market strength remained intact despite the modest pullback in the major indexes.

Total NYSE trading volume was 5,898,609,883 shares, a 6% decline from Tuesday’s volume of 6,254,852,082 shares. Although trading activity was lighter, overall market breadth and internal market statistics remained broadly consistent with those of the previous session.

NASDAQ: Advancing stocks also outnumbered declining stocks on the NASDAQ. The exchange recorded 2,661 advancers, 2,303 decliners, and 329 unchanged issues, producing an advancer-to-decliner ratio of approximately 1.15:1, reflecting modestly positive market breadth.

NASDAQ posted 350 new 52-week highs and 96 new 52-week lows, compared with 315 new highs and 161 new lows on Tuesday. The notable increase in new highs and sharp decline in new lows indicate that underlying market participation remained constructive, even as technology and semiconductor stocks experienced selling pressure.

Total NASDAQ trading volume amounted to 9,486,762,302 shares, approximately 8% lower than Tuesday’s 10,330,064,731 shares. The advancer-to-decliner ratio has moderated from approximately 3:2 (1.50:1) on Monday to 1.17:1 on Tuesday and 1.15:1 on Wednesday, suggesting that market breadth has gradually cooled while remaining positive. Overall, Wednesday’s session reflected consolidation rather than a significant shift in market direction.

Trading volume was also slightly below the NASDAQ’s 50-day average daily volume. From a technical standpoint, the Nasdaq Composite remains comfortably above its 50-day moving average and is currently trading near its 25-day moving average, indicating that the intermediate-term uptrend remains intact despite the day’s weakness.

.

Wednesday’s U.S. Market Wrap-Up Report

Wednesday’s trading session was characterized by a sharp rotation out of semiconductor, chip, and AI infrastructure stocks, while the broader market experienced only modest weakness. Although all four major U.S. equity indexes finished lower, declines outside the technology sector were relatively contained. The Dow Jones Industrial Average slipped just 0.03%, while the S&P 500 fell 0.22%. The Nasdaq Composite declined 0.66%, reflecting the heavy selling pressure in semiconductor and AI-related stocks.

Despite the weakness in the major indexes, market internals remained constructive. Both the NYSE and NASDAQ recorded more advancing than declining stocks, new 52-week highs continued to outnumber new lows by a wide margin, and trading volume on both exchanges declined from Tuesday’s levels. These statistics suggest that Wednesday’s selling was concentrated in a specific group of high-performing technology stocks rather than representing broad-based market liquidation.

Sector performance also reflected this rotation. Only three sectors closed higher. Financials led the market with a gain of 1.37%, followed by Consumer Discretionary (+0.50%) and Healthcare (+0.22%). On the downside, Industrials was the weakest-performing sector, falling 2.21%, followed by Utilities (-1.71%) and Technology (-1.09%). The relatively modest decline in the Technology sector masks the much steeper losses experienced within the semiconductor and AI infrastructure industries.

The biggest story of the session was the sharp pullback in semiconductor stocks after several months of exceptional gains. Many of Wednesday’s largest losers were among Tuesday’s strongest performers, suggesting profit-taking rather than a deterioration in the longer-term fundamentals.

Sandisk Corp. (SNDK), which surged 10.89% on Tuesday, fell 10.62% on Wednesday. Micron Technology (MU) declined 10.57% after posting a modest gain the previous day. Intel Corporation (INTC), Marvell Technology (MRVL), and Astera Labs Inc. (ALAB) also reversed Tuesday’s advances, falling 9.03%, 8.67%, and 10.80%, respectively. Trading volumes in these stocks remained elevated, indicating active institutional participation during the pullback.

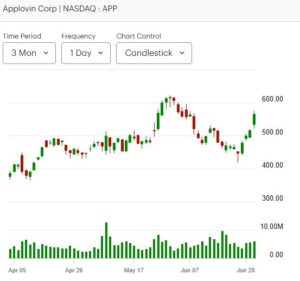

Not all technology stocks participated in the sell-off. Investors rotated into selected software and large-cap technology names. IBM gained 1.79%, MongoDB Inc. (MDB) advanced 6.99%, Snowflake Inc. (SNOW) rose 2.63%, Apple Inc. (AAPL) added 1.73%, and AppLovin Corp. (APP) climbed 9.58%. The strength in software and selected mega-cap technology companies suggests that investors were selectively reducing exposure to semiconductors rather than abandoning the technology sector altogether.

From a technical perspective, the broader market remains in a healthy position. The Nasdaq Composite continues to trade comfortably above its 50-day moving average and is testing support around its 25-day moving average. Likewise, the S&P 500 remains well above its 25-day, 50-day, and 200-day moving averages, indicating that the primary upward trend remains intact despite Wednesday’s weakness.

Key Takeaways for Traders and Investors

- Wednesday’s decline was primarily a sector-specific correction led by semiconductor and AI infrastructure stocks rather than a broad market sell-off.

- Market breadth remained positive on both the NYSE and NASDAQ, with advancing stocks outnumbering declining stocks and new 52-week highs continuing to exceed new lows. These are generally constructive internal market signals.

- Lower trading volume compared with Tuesday suggests there was no evidence of widespread institutional distribution across the broader market.

- After several months of exceptional gains, semiconductor stocks appear to be undergoing a period of profit-taking and consolidation. Such pullbacks are common following extended advances and can help establish healthier technical bases.

- Investors should monitor whether semiconductor stocks find support near key moving averages over the coming sessions. A stabilization in this group would reinforce the view that Wednesday’s decline was a normal correction within an ongoing bull trend.

- Unless selling pressure broadens significantly beyond semiconductors and AI-related stocks, the overall technical outlook for the U.S. equity market remains constructive.

.

NOTICE TO READERS

The Canadian Vanguard Stock Market is about empowering you to build and manage your wealth by yourself. There is certainly no magic in managing finances or wealth but one needs to know what to do and commit to doing what is needed. When you are ready to start the journey to Take Charge and Put Your Destiny In Your Own Hands, read The Canadian Vanguard every market day. If you need more related information, Contact Us

Our readers are strongly advised to conduct their own research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is no guarantee of future price appreciation. Any recommendation is not a guarantee of any particular stock’s future prices, and The Canadian Vanguard accepts no responsibility or liability for investors’ or readers’ purchases.

Stocks In The News/ Stocks To Watch and Market Strategy will soon be available only to Paying Subscribers. The dollar sign “$” in the Toronto Market section in the articles only stands for Canadian dollar and in the US market section “$” stands for US dollar.

(c) This article is published by The Canadian Vanguard on July 1, 2026