Canadian Wireless Providers Raise Prices, Reviving Investor Confidence

Canadian telecom stocks may be poised for a rebound after a two-year slump, as carriers start to stabilize wireless plan prices and make progress on debt reduction, analysts say.

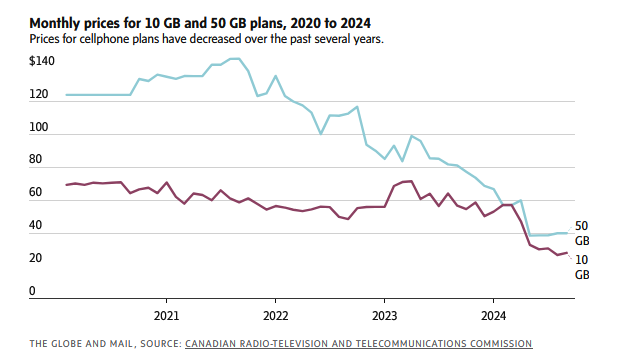

Over the last few years, telecom providers have ramped up competition in what has become a slow-growing, mature market, driven in part by the lower priced plans offered by Quebecor Inc.’s QBR-B-T Freedom Mobile.

But plan prices at main and flanker brands – lower-priced, secondary brands owned by the telecoms – have stabilized or even increased slightly in recent months, bucking the usual trend of discounting prices at the end of a financial quarter to boost subscriber numbers.

While average wireless prices are still down from 2023, analysts say the shift could lead to improved earnings potential over time.

Freedom Mobile, Rogers Communications Inc.’s RCI-B-T Fido, BCE Inc.’s BCE-T Virgin Plus and Telus Corp.’s T-T Koodo all raised rates in recent weeks, according to Bank of Nova Scotia analyst Maher Yaghi.

Still, telecoms are earning less per customer than they have in previous years. Mr. Yaghi estimates that more than half of Canadian wireless subscribers have switched to cheaper plans in recent years. This reduces average revenue per user, or ARPU, a key profitability metric.

As telecoms report year-over-year wireless ARPU declines, “what percentage of their base has repriced at the lower pricing levels is a focus for investors,” said Canadian Imperial Bank of Commerce analyst Stephanie Price in a note to investors.

“We see valuation upside at current levels, although we expect that it will take several years for the Canadian telecom customer base to completely reprice,” she added.

Desjardins analyst Jérome Dubreuil cautioned that ARPU recovery could take some time, but said he believes the industry valuation multiples are “bottoming,” making the sector more appealing to investors who have avoided it for the last two years.

Royal Bank of Canada analyst Drew McReynolds shared the view, saying he believes the telecom sector “has now moved beyond the trough,” and that the companies look more likely to achieve the mid-points of their guidance ranges for the year, though he sees “a still subdued growth outlook” for the sector.

Stock prices for all four of the country’s largest telecoms have bounced back in recent weeks, following a difficult 2024. Since mid-June, stock in Bell Canada parent BCE Inc. is up 5 per cent; Telus is up 3 per cent; and Quebecor is up 1.5 per cent. Rogers is up 21 per cent, after the closing of its $4.7-billion deal to buy BCE’s stake in Maple Leaf Sports and Entertainment on July 2.

The four telecoms will release quarterly earnings in the coming weeks.

Analysts are expecting updates to various deals and possible divestitures, including the potential sale of a minority stake in MLSE by Rogers, a potential tower sale by Telus and an update on the close of BCE’s $1-billion Northwestel divestiture.

Mr. McReynolds said he thinks Rogers and Telus will be the only telecoms to deliver positive year-over-year consolidated revenue growth in the quarter.

Both companies have taken recent steps to strengthen their balance sheets.

After the closing of a $7-billion backhaul deal, last week Rogers launched two cash offers to repurchase up to US$1.25-billion and $400-million of outstanding senior notes.

And Telus recently raised US$1.5-billion through the issuance of long-term junior subordinated notes to fund tender offers, reduce debt and support general corporate purposes, the company said.

Mr. McReynolds expects Quebecor to lead on wireless subscribers in the quarter, projecting it will have added 70,000 net new customers. The company won 54,400 last quarter – approximately 45 per cent of all new wireless customers in Canada.

He expects growth headwinds for BCE in the near-term but sees a medium-turn uptick for the stock, given the recent dividend cut and the company’s May announcement that it would bring in partner PSP Investments to help fund the expansion of its U.S. acquisition Ziply Fiber.

Aravinda Galappatthige, analyst at Canaccord Genuity, told investors he believes BCE is positioned to return to a low single-digit growth trajectory, partially owing to the prospect of further divestitures being announced during the second half of 2025.

This article was first reported by The Globe and Mail