Stock Markets Rebound as Iran and Israel Halt Attacks, Easing Geopolitical Fears

The Canadian Vanguard Stock Market Report Monday June 8, 2026 Edition

.

The Toronto Market

Monday’s Toronto Market Index

The S&P/TSX Composite Index gained 65.29 points, or 0.19%, to close at 34,478.74 on Monday. While the index recovered modestly following Friday’s sharp 2.28% decline, the rebound was relatively muted.

The TSX opened higher but remained well below Friday’s high and ultimately finished the session significantly below its intraday peak, indicating a lack of strong buying momentum. Encouragingly, Monday’s low was above both Friday’s low and Friday’s closing level, suggesting that downside pressure may be easing.

Despite today’s gain, considerable ground remains to be recovered from Friday’s sell-off. However, current price action suggests that the weakness was more likely driven by profit-taking after a strong advance rather than by widespread panic selling. Continued stabilization over the next several sessions would help reinforce that view.

Monday’s TSX Market Statistics

Market breadth on the TSX was positive on Monday, with advancing issues outnumbering declining issues. There were 1,282 advancers versus 985 decliners, resulting in an advancer-to-decliner ratio of 1.30-to-1, or roughly six advancing stocks for every five declining stocks. An additional 151 issues closed unchanged. While the positive breadth reflects a generally constructive tone, the margin of outperformance by advancers was not particularly strong given the magnitude of Friday’s sell-off.

The TSX recorded 76 new 52-week highs and 32 new 52-week lows. Although new highs comfortably exceeded new lows, the number of stocks reaching fresh highs remained well below the 207 new highs recorded before Friday’s decline. This suggests that leadership narrowed following the market setback and that many stocks have yet to regain their upward momentum.

Total TSX trading volume was 480.2 million shares, down 5% from the 504.6 million shares traded on Friday. Friday’s session was characterized by elevated trading activity as investors reacted to the sharp market decline, whereas Monday’s volume returned to a level more consistent with the 25-day average. The reduction in volume indicates that selling pressure subsided, but it also suggests that buyers were not particularly aggressive in chasing stocks higher.

Taken together, Monday’s statistics point to a market that is stabilizing after Friday’s sharp decline rather than one that is mounting a strong recovery. Positive breadth and a favorable new-high/new-low ratio are encouraging signs, but the relatively modest number of new 52-week highs and average trading volume indicate that investor confidence remains somewhat cautious.

Takeaway for Traders and Investors

Monday’s session can best be described as a constructive pause following Friday’s significant sell-off. The positive market breadth suggests that buyers returned to the market, but the lack of strong volume and the sharp drop in new 52-week highs indicate that conviction remains limited.

For traders, the key question is whether breadth and momentum continue to improve over the next several sessions. Sustained gains accompanied by rising volume and an expanding list of new highs would signal that Friday’s decline was primarily a profit-taking event. Conversely, if rallies continue to occur on average or below-average volume while new highs remain subdued, it may indicate that investors are still assessing risk and that a more prolonged consolidation phase is likely.

At this stage, the evidence favors a market that is attempting to rebuild its footing, but confirmation of renewed upside momentum is still needed.

Monday’s Toronto Market Wrap-Up Report

The S&P/TSX Composite Index gained 0.19% on Monday, a modest recovery following Friday’s sharp 2.28% decline. While the gain was relatively small, the market’s ability to avoid a second consecutive day of heavy selling was an encouraging development. However, the session fell well short of a meaningful rebound, indicating that investors remain cautious after Friday’s setback.

Market participation was mixed, with only five of the TSX’s ten major sectors finishing in positive territory. Technology led the advance, rising 0.59%, followed by Energy (+0.41%) and Financials (+0.25%). On the downside, Utilities fell 1.07%, while Consumer Durables & Services declined 1.40%, making them the weakest-performing sectors of the day.

The lack of a stronger recovery suggests that investors are still evaluating whether Friday’s sell-off represented a healthy bout of profit-taking or the beginning of a deeper corrective phase. The fact that the TSX failed to reclaim a meaningful portion of Friday’s losses points to a market that is stabilizing rather than aggressively buying the dip.

Technology stocks were among the hardest hit sectors during Friday’s decline and managed to recover only a fraction of those losses on Monday. Support came primarily from Shopify Inc., which gained 1.22%, and Celestica Inc., which added 0.93%. Despite the sector’s leadership, the rebound was not broad enough to signal a decisive return of risk appetite.

Among individual stocks, Celestica Inc. (CLS) staged a notable recovery, rising 3.80% to close at $538.27 on volume of 373,500 shares. Nevertheless, the stock remains significantly below Thursday’s close of $636.06, highlighting the severity of last week’s decline. Investors who entered the stock near recent highs continue to face substantial unrealized losses, while traders will be watching closely for evidence that support is forming.

Badger Infrastructure Solutions Ltd. (BDGI) was one of the day’s strongest performers, advancing 5.73% to close at $93.69 after receiving favorable analyst commentary. Cameco Corp. also posted a solid gain of 1.96%, closing at $146.91 on volume of 650,200 shares.

Interestingly, some of the market’s strongest performers in recent months failed to participate in Monday’s advance. Wheaton Precious Metals Corp. declined 1.07% to $160.15 despite above-average trading activity, while Franco-Nevada Corp. fell 1.72% to $299.41. Weakness among precious metals stocks during an up day for the broader market may suggest some ongoing rotation away from defensive areas and toward cyclical sectors.

Energy and mining names delivered mixed results. Suncor Energy Inc. gained 1.47%, while Lundin Mining Corp. rose 2.26% to close at $38.06 on robust volume of 3.1 million shares, reflecting continued investor interest in economically sensitive sectors.

Takeaway for Investors

Monday’s session provided evidence that Friday’s sharp decline did not trigger widespread panic selling. Market breadth was positive, major sectors avoided broad-based liquidation, and trading volume returned to more normal levels. These are characteristics typically associated with profit-taking rather than the start of a major bear-market decline.

That said, investors should not mistake stabilization for renewed strength. The TSX recovered only a small fraction of Friday’s losses, sector participation was limited, and the number of stocks making new highs remained subdued. The market still has significant technical damage to repair before a convincing bullish outlook can be restored.

For now, the evidence favors a market attempting to stabilize after a sharp shakeout. The next several trading sessions will be critical in determining whether Friday’s decline was merely a pause within an ongoing bull trend or the beginning of a more prolonged corrective period.

.

The US Markets

Monday’s U.S. Market Indexes

U.S. equities delivered a mixed performance on Monday as investors balanced renewed strength in technology stocks against rising geopolitical concerns in the Middle East.

The Dow Jones Industrial Average slipped 80.77 points, or 0.16%, to close at 50,786.01. The S&P 500 gained 21.99 points, or 0.30%, ending the session at 7,405.73, while the Nasdaq Composite advanced 220.23 points, or 0.86%, to close at 25,929.66. The Russell 2000 Index rose 21.92 points, or 0.77%, finishing the day at 2,855.42.

Technology stocks, particularly semiconductor and AI infrastructure names, once again provided the leadership necessary for the Nasdaq and S&P 500 to recover a portion of Friday’s losses. Investor demand remained concentrated in growth-oriented sectors, reflecting continued confidence in long-term artificial intelligence spending trends despite broader market uncertainty.

The Russell 2000 initially outperformed during the morning session, at one point rising nearly 50 points above Friday’s close. However, much of that gain evaporated during afternoon trading as geopolitical headlines concerning the Iran-Israel conflict heightened risk aversion. The index later attempted to recover but ultimately closed well below its intraday high, suggesting that investors remained reluctant to maintain aggressive exposure to economically sensitive small-cap stocks.

Large-cap industrial and cyclical stocks within the Dow Jones Industrial Average also displayed relative weakness as investors assessed the potential economic implications of escalating tensions in the Middle East. Financial markets have become increasingly sensitive to developments that could disrupt global energy supplies or place upward pressure on commodity prices.

A primary concern for investors is the potential inflationary impact of sustained increases in oil prices. Higher energy costs can feed into broader inflation measures, complicating the Federal Reserve’s efforts to maintain price stability. If inflationary pressures were to reaccelerate, expectations for future monetary easing could diminish, and in an extreme scenario, the possibility of additional policy tightening could re-enter market discussions.

Market Takeaway

Monday’s trading action reinforced a theme that has dominated much of this year’s market advance: technology continues to carry the broader market. The Nasdaq and S&P 500 were able to post gains largely because investors remained committed to semiconductor, AI infrastructure, and large-cap technology leaders.

However, beneath the surface, market action was less convincing. The Dow Jones declined, small-cap stocks surrendered much of their intraday gains, and investors demonstrated increased sensitivity to geopolitical developments. This divergence suggests that risk appetite remains selective rather than broad-based.

The market’s ability to sustain its recovery may depend on whether leadership broadens beyond technology. A healthy bull market typically requires participation from financials, industrials, consumer discretionary stocks, and small-cap companies. Until that occurs, market gains may remain vulnerable to shifts in sentiment and external shocks.

🔒 Premium Content

You must be a subscriber to access the remaining parts of this section. Current subscription rate is $60 CAD for a year

Monday’s U.S. Market Statistics

New York Stock Exchange (NYSE): Market breadth on the NYSE was essentially neutral on Monday, with declining issues narrowly exceeding advancing issues. The exchange recorded 2,230 decliners and 2,203 advancers, while 425 issues finished unchanged. This resulted in a decliner-to-advancer ratio of approximately 1.01-to-1, indicating a market that remained evenly divided between buyers and sellers despite the mixed performance of the major indexes.

The NYSE recorded 129 new 52-week highs and 162 new 52-week lows. While new lows continued to outnumber new highs, the gap narrowed significantly from Friday’s readings of 132 new highs and 249 new lows. This improvement suggests that downside pressure eased considerably following Friday’s broad market sell-off.

Total NYSE trading volume reached 5.01 billion shares, down 12% from the 5.70 billion shares traded on Friday. The decline in volume indicates that Friday’s elevated trading activity was likely driven by liquidation and profit-taking, while Monday’s session reflected a more measured and less emotional market environment.

Overall, NYSE statistics point to a market that is stabilizing after Friday’s weakness but has not yet demonstrated sufficient strength to signal a decisive recovery.

NASDAQ: Market breadth was notably stronger on the NASDAQ, where advancing stocks outnumbered declining stocks by a healthy margin. The exchange recorded 2,746 advancers and 2,142 decliners, resulting in an advancer-to-decliner ratio of 1.28-to-1, with an additional 391 issues closing unchanged.

The positive breadth helped support the Nasdaq Composite’s 0.86% gain and reflected continued investor interest in growth-oriented sectors, particularly technology, semiconductors, and artificial intelligence infrastructure stocks. Although the Nasdaq recovered a portion of Friday’s decline, the rebound represented only a modest step toward repairing the technical damage inflicted during the previous session.

The NASDAQ posted 149 new 52-week highs and 195 new 52-week lows, compared with 124 new highs and 290 new lows on Friday. This was a meaningful improvement in internal market conditions, as new lows declined sharply while new highs increased. Nevertheless, new lows still exceeded new highs, indicating that the recovery remains incomplete.

Total NASDAQ trading volume amounted to 10.58 billion shares, down 12% from Friday’s 11.97 billion shares. The lower volume suggests that while selling pressure subsided, institutional investors have not yet returned with the conviction typically associated with a strong market rebound.

What the Statistics Are Telling Us

Monday’s market statistics reveal a market attempting to regain its footing after Friday’s sharp decline.

The NYSE showed signs of stabilization, but breadth remained essentially neutral and new lows continued to outnumber new highs. In contrast, the NASDAQ exhibited stronger internal strength, supported by positive breadth and an improving new-high/new-low profile. Technology-related sectors continued to attract buying interest and were largely responsible for the Nasdaq Composite’s outperformance.

However, neither exchange produced the type of broad-based participation typically associated with a powerful recovery rally. Trading volume declined significantly on both exchanges, suggesting that buyers remain cautious and that institutional investors are still assessing market conditions.

For now, the statistics suggest that Friday’s sell-off may have been more consistent with profit-taking than the beginning of a major market downturn. However, traders and investors should look for stronger breadth, rising volume, and expanding new highs before concluding that the market has fully regained its upward momentum.

Monday’s U.S. Market Wrap-Up Report

U.S. equity markets delivered a mixed performance on Monday as investors balanced improving geopolitical developments against lingering concerns about inflation, interest rates, and the broader market impact of recent volatility.

Market sentiment improved late in the day after both Iran and Israel indicated that they would halt military attacks against one another. The announcement followed calls from President Trump urging both sides to de-escalate tensions. Financial markets generally respond favorably to reductions in geopolitical risk, and futures traded modestly higher following the news. If the ceasefire holds, investors could enter Tuesday’s session with a more constructive outlook and a greater willingness to assume risk.

The major indexes closed mixed. The Dow Jones Industrial Average declined, while the S&P 500 and Nasdaq Composite posted gains, led by renewed strength in technology and semiconductor stocks. Commodity markets also reflected a moderation in risk concerns, with crude oil falling 0.83% and gold edging lower by 0.07% at the time this report was prepared.

Technology stocks were once again the primary source of market leadership. Semiconductor and AI-related companies recovered a meaningful portion of Friday’s losses as investors returned to growth-oriented sectors. SanDisk Corporation gained 5.3%, while Micron Technology surged 9.8%, making it one of the strongest performers within the semiconductor group. Astera Labs advanced 9.23%, reflecting continued investor enthusiasm for companies tied to artificial intelligence infrastructure and data center spending.

Broadcom Inc. (AVGO) rose 2.8%, recovering some of the sharp decline that followed last week’s earnings report. Although Broadcom delivered solid results, investors reacted negatively to management’s revenue outlook, leading to significant selling pressure. Monday’s rebound suggests that bargain hunters and longer-term investors may be beginning to view the recent weakness as an opportunity.

For Broadcom (AVGO ) stock, recovery or repair may take sometime.

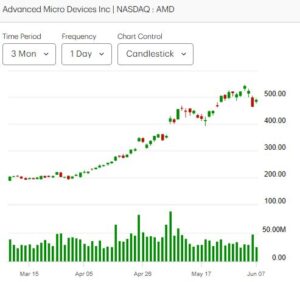

Advanced Micro Devices (AMD) gained 5.1% and appears well positioned to recover most, if not all, of Friday’s decline should market conditions remain supportive. Strength also extended beyond semiconductors, with data storage companies Seagate Technology and Western Digital both posting gains as investors selectively returned to technology hardware names.

Among individual corporate developments, Intel was one of the market’s standout performers, surging 11% and leading the S&P 500 for the session. The rally followed news that Intel is expanding its partnership with Cadence Design Systems to accelerate development of next-generation semiconductor technologies. While Intel remains in the midst of a long-term turnaround effort, Monday’s move reflected growing optimism regarding its strategic positioning.

Connectivity and infrastructure-related companies also participated in the recovery. Corning gained 5.6% after Amazon.com announced a multibillion-dollar agreement with the company to provide connectivity solutions supporting hyperscale data center infrastructure. Lumentum Holdings rose 3.7%, while Coherent advanced 6.6%. Notably, all three stocks had declined more than 8% during Friday’s sell-off, highlighting the degree of bargain hunting that emerged during Monday’s session.

🔒 Premium Content

You must be a subscriber to access the remaining parts of this section. Current subscription rate is $60 CAD for a year

For traders and investors, the key message from Monday’s session is that buyers remain highly committed to the artificial intelligence, semiconductor, and data center investment themes that have powered much of the market’s advance. If geopolitical risks continue to recede and inflation expectations remain contained, the market may be positioned to recover additional ground from Friday’s sell-off. The next few sessions should provide important clues as to whether Monday marked the beginning of a sustainable rebound or merely a temporary relief rally.

.

NOTICE TO READERS

The Canadian Vanguard Stock Market is about empowering you to build and manage your wealth by yourself. There is certainly no magic in managing finances or wealth but one needs to know what to do and commit to doing what is needed. When you are ready to start the journey to Take Charge and Put Your Destiny In Your Own Hands, read The Canadian Vanguard every market day. If you need more related information, Contact Us

Our readers are strongly advised to conduct their own research into individual stocks before making a purchase decision. In addition, investors are advised that past stock performance is no guarantee of future price appreciation. Any recommendation is not a guarantee of any particular stock’s future prices, and The Canadian Vanguard accepts no responsibility or liability for investors’ or readers’ purchases.

Stocks In The News/ Stocks To Watch and Market Strategy will soon be available only to Paying Subscribers. The dollar sign “$” in the Toronto Market section in the articles only stands for Canadian dollar and in the US market section “$” stands for US dollar.

(c) This article is published by The Canadian Vanguard on June 8, 2026